Key Events This Week

1 June: Strong Q4 FY26 results announced amid valuation concerns

2 June: Quarterly turnaround confirmed with record revenue and profit

2 June: Quality grade downgraded highlighting fundamental challenges

5 June: Week closes at Rs.6.89, up 2.07% for the week

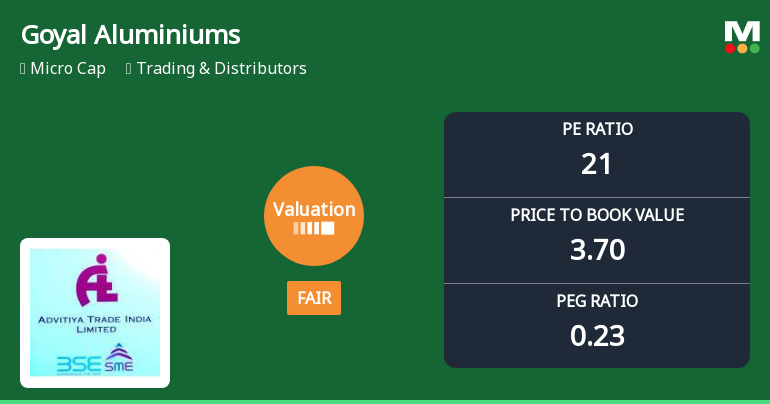

Goyal Aluminiums Ltd Valuation Shifts to Fair Amid Mixed Market Performance

2026-06-12 08:00:59Goyal Aluminiums Ltd, a micro-cap player in the Trading & Distributors sector, has witnessed a notable shift in its valuation parameters, moving from an expensive to a fair valuation grade. This change, reflected in key metrics such as the price-to-earnings (P/E) and price-to-book value (P/BV) ratios, suggests a more attractive entry point for investors despite recent share price declines and a Sell mojo grade upgrade from Strong Sell.

Read full news article

Goyal Aluminiums Ltd is Rated Sell

2026-06-04 10:10:04Goyal Aluminiums Ltd is rated 'Sell' by MarketsMOJO, with this rating last updated on 01 June 2026. However, the analysis and financial metrics discussed here reflect the stock's current position as of 04 June 2026, providing investors with the latest insights into the company’s performance and outlook.

Read full news article