Valuation Picture: Discount Amidst Sector Premiums

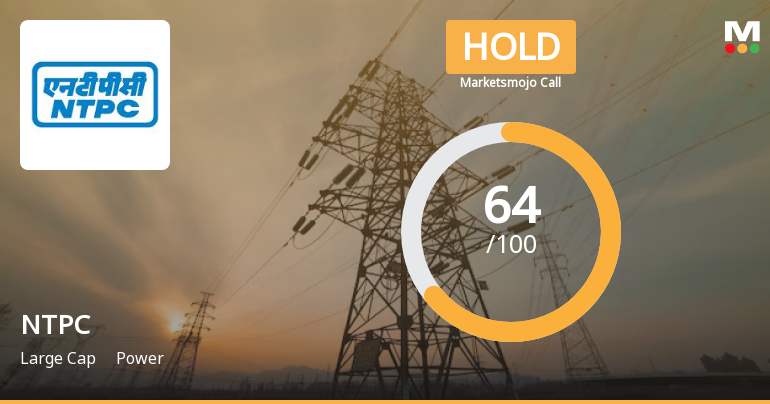

NTPC Ltd. trades at a P/E of 12.05, markedly below the power sector’s average of 22.75. This 47% discount suggests the market is pricing in either subdued growth expectations or elevated risks relative to peers. Such a valuation gap is notable given the company’s large-cap status with a market capitalisation of ₹3,32,401.72 crores. The sector’s elevated P/E reflects optimism around power generation and distribution companies, yet NTPC Ltd. remains priced conservatively. This divergence raises the question of whether the discount i...

Read full news article