Key Events This Week

May 25: Stock opens steady at Rs.130.70 despite Sensex rally

May 27: Sharp quarterly results trigger 8.19% drop to Rs.120.00

May 29: Continued selling pressure leads to 10.62% fall, closing at Rs.107.25

Aug 04, 03:30 PM

BSE+NSE Vol: 12000

Silky Overseas Ltd is rated Strong Sell by MarketsMOJO. This rating was last updated on 01 June 2026, reflecting a significant reassessment of the stock’s outlook. However, all fundamentals, returns, and financial metrics discussed here are current as of 22 July 2026, providing investors with the latest perspective on the company’s position.

Read full news article

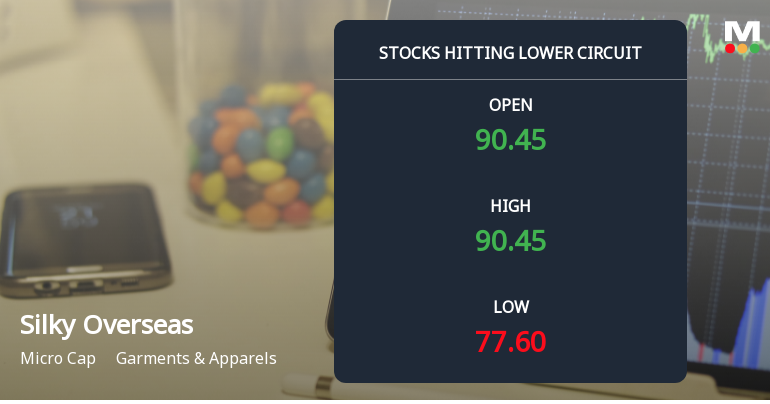

At Rs 77.6, sellers were still queuing — but there were no buyers willing to take the other side. Silky Overseas Ltd locked at its lower circuit of 20.0% on 17 Jul 2026, with unfilled sell orders and a frozen price that capped losses for the day.

Read full news article

Silky Overseas Ltd is rated Strong Sell by MarketsMOJO, with this rating last updated on 01 June 2026. However, the analysis and financial metrics discussed here reflect the stock’s current position as of 09 July 2026, providing investors with the latest insights into the company’s performance and outlook.

Read full news article

Silky Overseas Ltd is rated Strong Sell by MarketsMOJO, with this rating last updated on 01 June 2026. However, the analysis and financial metrics discussed here reflect the stock’s current position as of 28 June 2026, providing investors with the latest insights into the company’s performance and outlook.

Read full news article

Silky Overseas Ltd is rated Strong Sell by MarketsMOJO. This rating was last updated on 01 June 2026, reflecting a significant reassessment of the stock’s outlook. However, all fundamentals, returns, and financial metrics discussed here are current as of 17 June 2026, providing investors with the latest perspective on the company’s position.

Read full news article

Silky Overseas Ltd is rated Strong Sell by MarketsMOJO, with this rating last updated on 01 June 2026. However, the analysis and financial metrics discussed here reflect the stock’s current position as of 04 June 2026, providing investors with the most up-to-date view of the company’s fundamentals, valuation, financial trends, and technical outlook.

Read full news article

May 25: Stock opens steady at Rs.130.70 despite Sensex rally

May 27: Sharp quarterly results trigger 8.19% drop to Rs.120.00

May 29: Continued selling pressure leads to 10.62% fall, closing at Rs.107.25

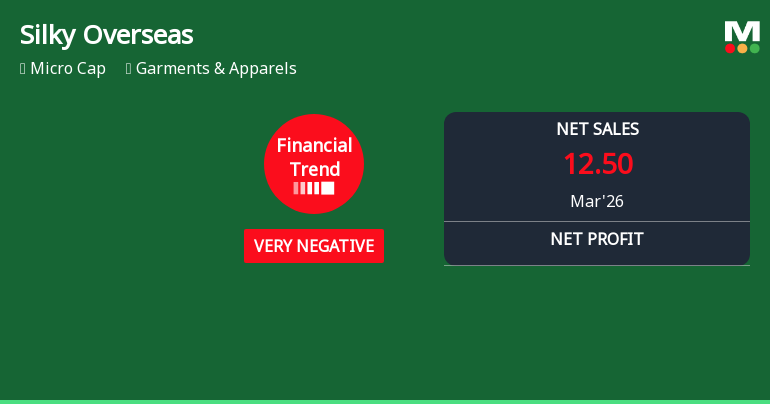

Silky Overseas Ltd, a micro-cap player in the Garments & Apparels sector, has reported a markedly deteriorated financial performance for the quarter ended March 2026, signalling a significant shift from its previously flat trend to a very negative trajectory. The company’s latest quarterly results reveal steep declines across key metrics including revenue, profitability, and margins, raising concerns about its near-term outlook amid challenging market conditions.

Read full news articleSilky Overseas Ltd's latest financial results for the quarter ending March 2026 reveal significant operational challenges. The company reported net sales of ₹12.50 crores, marking a sharp decline of 61.05% from the previous quarter and a 47.17% decrease year-on-year. This represents the lowest sales figure in the past seven quarters, indicating a concerning trend in revenue generation. The net profit for the same quarter turned negative at ₹0.61 crores, a stark contrast to the profit of ₹2.39 crores recorded in the prior quarter. This shift reflects a deterioration in profitability, with the company experiencing a negative profit margin of 4.88%, which is also the lowest observed in the dataset. The operating margin fell to 2.40%, down from 13.31% in the previous quarter, highlighting severe margin compression and operational inefficiencies. The financial performance indicates that Silky Overseas is facin...

Read full news article

No Upcoming Board Meetings

No Dividend history available

No Splits history available

No Bonus history available

No Rights history available