Key Events This Week

3 Aug: Stock opens at Rs.1,951.00, declines 1.02% amid broad market gains

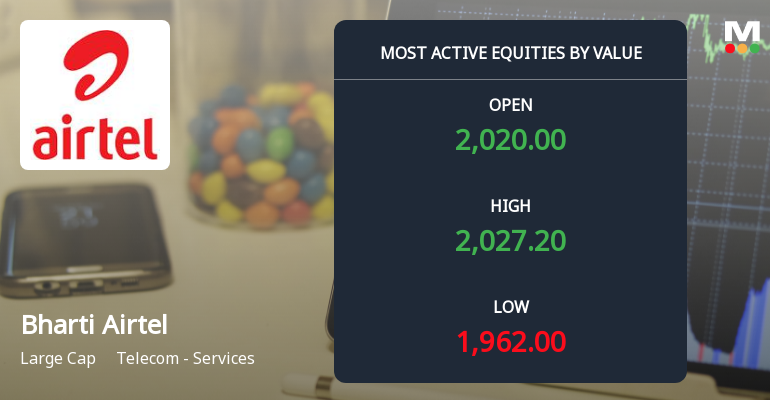

4 Aug: High-value trading with Rs.184.09 crore turnover; MarketsMOJO upgrades rating to Hold

5 Aug: Surge in call and put option activity ahead of 25 Aug expiry

7 Aug: Technical momentum shifts to mildly bullish with positive weekly indicators

Week Open

Rs.1,971.15

Read full news article