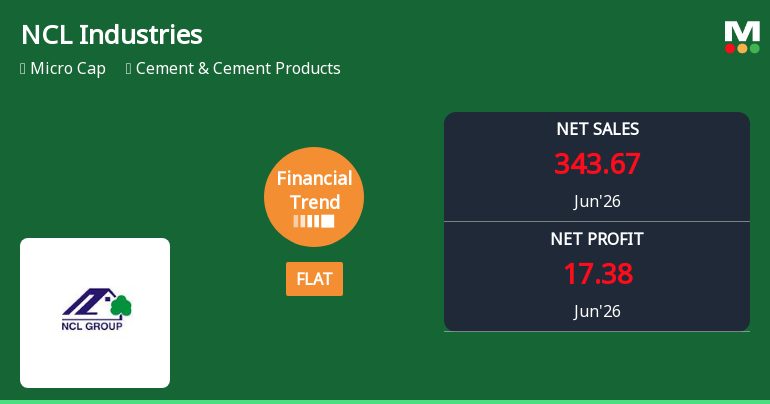

NCL Industries Ltd Reports Flat Quarterly Performance Amid Margin Pressures

2026-08-10 08:00:27NCL Industries Ltd, a micro-cap player in the Cement & Cement Products sector, reported a flat financial performance for the quarter ended June 2026, signalling a marked slowdown from its previously very positive trend. Despite some operational strengths, the company’s profitability and margin metrics have deteriorated, prompting a downgrade in its Mojo Grade from Hold to Sell as of 29 May 2026.

Read full news article

NCL Industries Ltd is Rated Hold by MarketsMOJO

2026-08-06 10:11:23NCL Industries Ltd is rated 'Hold' by MarketsMOJO, with this rating last updated on 29 May 2026. However, the analysis and financial metrics discussed here reflect the stock's current position as of 06 August 2026, providing investors with an up-to-date view of the company’s fundamentals, returns, and market standing.

Read full news articleWhen is the next results date for NCL Industries Ltd?

2026-08-03 23:16:38The next results date for NCL Industries Ltd is scheduled for 07 August 2026....

Read full news article

NCL Industries Ltd is Rated Hold

2026-07-26 10:10:16NCL Industries Ltd is rated 'Hold' by MarketsMOJO, with this rating last updated on 29 May 2026. However, the analysis and financial metrics discussed here reflect the stock's current position as of 26 July 2026, providing investors with the latest insights into its performance and outlook.

Read full news article

NCL Industries Ltd is Rated Hold by MarketsMOJO

2026-07-15 10:11:02NCL Industries Ltd is rated 'Hold' by MarketsMOJO, with this rating last updated on 29 May 2026. While the rating change occurred on that date, the analysis and financial metrics discussed here reflect the stock's current position as of 15 July 2026, providing investors with an up-to-date perspective on the company’s performance and outlook.

Read full news article

NCL Industries Ltd is Rated Hold by MarketsMOJO

2026-07-04 10:10:33NCL Industries Ltd is rated 'Hold' by MarketsMOJO, with this rating last updated on 29 May 2026. However, the analysis and financial metrics discussed here reflect the company’s current position as of 04 July 2026, providing investors with the latest insights into its performance and outlook.

Read full news article

NCL Industries Ltd is Rated Hold by MarketsMOJO

2026-06-23 10:10:54NCL Industries Ltd is rated 'Hold' by MarketsMOJO, with this rating last updated on 29 May 2026. However, the analysis and financial metrics presented here reflect the stock's current position as of 23 June 2026, providing investors with an up-to-date view of the company’s fundamentals, returns, and market standing.

Read full news article

NCL Industries Ltd Technical Momentum Shifts Amid Mixed Market Signals

2026-06-23 08:06:31NCL Industries Ltd, a micro-cap player in the Cement & Cement Products sector, has experienced a notable shift in its technical momentum, moving from a sideways trend to a mildly bearish stance. Despite a recent upgrade in its Mojo Grade from Sell to Hold, the stock’s technical indicators present a complex picture, with mixed signals from MACD, RSI, moving averages, and other momentum oscillators. This analysis delves into the latest technical parameters, price action, and comparative returns to provide investors with a comprehensive view of the stock’s current positioning.

Read full news article

NCL Industries Ltd Technical Momentum Shifts Amid Cement Sector Dynamics

2026-06-17 08:05:20NCL Industries Ltd has exhibited a notable shift in its technical momentum, moving from a mildly bearish stance to a more neutral sideways trend. This transition is underscored by mixed signals from key technical indicators such as MACD, RSI, Bollinger Bands, and moving averages, reflecting a complex interplay of market forces within the cement sector.

Read full news articleCorporate Action- Record Date For Final Dividend

07-Aug-2026 | Source : BSEDear Sir/Madam

Board Meeting Outcome for Outcome Of Board Meeting

07-Aug-2026 | Source : BSEDear Sir/Madam

45TH AGM- Book Closure

07-Aug-2026 | Source : BSEDear Sir

Corporate Actions

No Upcoming Board Meetings

NCL Industries Ltd has declared 15% dividend, ex-date: 20 Feb 26

No Splits history available

No Bonus history available

NCL Industries Ltd has announced 4:5 rights issue, ex-date: 27 Feb 06