Roadstar Infra Investment Trust is Rated Strong Sell

2026-07-17 10:10:23Roadstar Infra Investment Trust is rated Strong Sell by MarketsMOJO, with this rating last updated on 03 July 2026. However, the analysis and financial metrics presented here reflect the stock's current position as of 17 July 2026, providing investors with the most up-to-date view of the company’s fundamentals, returns, and overall outlook.

Read full news article

Roadstar Infra Investment Trust Sees Mild Shift in Technical Momentum Amid Mixed Returns

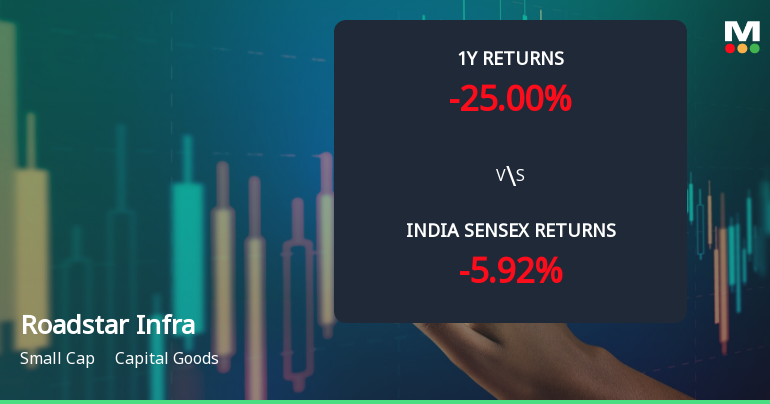

2026-07-14 08:07:03Roadstar Infra Investment Trust has experienced a notable shift in its technical parameters, reflecting a nuanced change in price momentum. Despite a recent uptick in its share price to ₹60.00, the stock remains under pressure with a Strong Sell mojo grade, highlighting the challenges faced by investors amid mixed technical signals and a bearish longer-term outlook.

Read full news article

Roadstar Infra Investment Trust Faces Bearish Technical Shift Amidst Mixed Returns

2026-07-08 08:06:40Roadstar Infra Investment Trust’s technical indicators have shifted decisively towards a bearish outlook, signalling a challenging phase ahead for this small-cap stock. Despite a stable current price of ₹57.75, the stock’s momentum and key technical parameters suggest increased downside risks, prompting a strong sell rating from MarketsMOJO.

Read full news article

Roadstar Infra Investment Trust Downgraded to Strong Sell Amid Deteriorating Fundamentals and Bearish Technicals

2026-07-06 08:19:44Roadstar Infra Investment Trust has been assigned a Strong Sell rating with a Mojo Score of 17.0, reflecting a significant downgrade from its previous ungraded status. This change, effective from 03 July 2026, is driven primarily by deteriorating technical indicators, weak financial trends, and a complex valuation profile that presents both risks and opportunities for investors.

Read full news article

Roadstar Infra Investment Trust Faces Bearish Momentum Amid Technical Downgrade

2026-07-06 08:04:31Roadstar Infra Investment Trust has undergone a significant technical parameter change, shifting its trend classification from neutral to bearish. Despite a modest intraday price gain, key momentum indicators and moving averages signal a deteriorating outlook, prompting a strong sell rating from MarketsMOJO.

Read full news article

Roadstar Infra Investment Trust Valuation Shifts to Very Attractive Amid Market Volatility

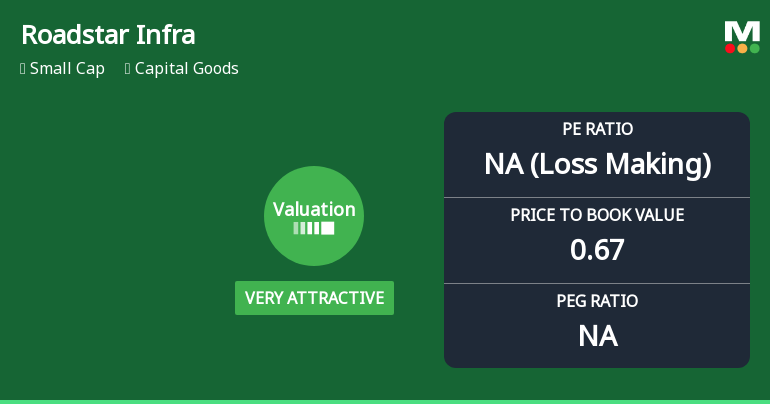

2026-07-06 08:01:59Roadstar Infra Investment Trust has seen a significant shift in its valuation parameters, moving from a risky to a very attractive investment grade. Despite a modest day change of 0.43%, the stock’s price-to-earnings (P/E) ratio and price-to-book value (P/BV) metrics suggest a compelling opportunity for value-focused investors amid a challenging market backdrop.

Read full news article

Roadstar Infra Investment Trust is Rated Strong Sell

2026-07-04 10:10:04Roadstar Infra Investment Trust is rated Strong Sell by MarketsMOJO. This rating was last updated on 03 July 2026, reflecting a comprehensive assessment of the stock’s current position. However, all fundamentals, returns, and financial metrics discussed below are as of 04 July 2026, providing investors with the most up-to-date view of the company’s performance and outlook.

Read full news article

Roadstar Infra Investment Trust is Rated Sell

2026-06-21 10:10:03Roadstar Infra Investment Trust is rated Sell by MarketsMOJO. This rating was last updated on 11 June 2026, reflecting a reassessment of the stock’s outlook. However, all fundamentals, returns, and financial metrics discussed here are current as of 21 June 2026, providing investors with the latest view of the company’s position in the market.

Read full news article

Roadstar Infra Investment Trust is Rated Strong Sell

2026-06-10 10:10:27Roadstar Infra Investment Trust is rated Strong Sell by MarketsMOJO. This rating was last updated on 05 June 2026, reflecting a reassessment of the stock’s outlook. However, all fundamentals, returns, and financial metrics discussed here are current as of 10 June 2026, providing investors with the latest view of the company’s position in the market.

Read full news articleReg 23(5)(g): Outcome of Unitholder meetings

17-Jul-2026 | Source : BSERoadstar Infra Investment Trust has informed the Exchange regarding Outcome of Annual General Meeting held on 17/07/2026

Reg 23(5)(i): Disclosure of material issue

13-Jul-2026 | Source : BSERoadstar Infra Investment Trust has informed the Exchange regarding Disclosure of material issue

Reg 23(5)(i): Disclosure of material issue

10-Jul-2026 | Source : BSERoadstar Infra Investment Trust has informed the Exchange regarding Disclosure of material issue

Corporate Actions

No Upcoming Board Meetings

Roadstar Infra Investment Trust has declared 5% dividend, ex-date: 29 May 26

No Splits history available

No Bonus history available

No Rights history available