Scoda Tubes Ltd is Rated Sell

2026-08-04 10:10:04Scoda Tubes Ltd is rated 'Sell' by MarketsMOJO, with this rating last updated on 18 May 2026. However, the analysis and financial metrics discussed here reflect the stock's current position as of 04 August 2026, providing investors with an up-to-date perspective on the company’s performance and outlook.

Read full news article

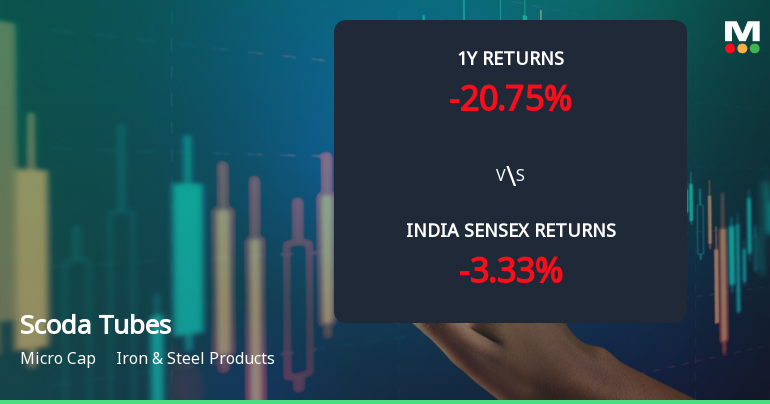

Scoda Tubes Ltd Technical Momentum Shifts Amid Mixed Market Returns

2026-08-04 08:11:34Scoda Tubes Ltd, a micro-cap player in the Iron & Steel Products sector, has experienced a notable shift in its technical momentum, moving from a mildly bearish stance to a sideways trend. Despite a modest day gain of 2.05%, the stock’s broader technical indicators present a complex picture, reflecting mixed signals that investors should carefully analyse amid challenging market conditions.

Read full news article

Scoda Tubes Ltd is Rated Sell

2026-07-24 10:10:19Scoda Tubes Ltd is rated 'Sell' by MarketsMOJO, with this rating last updated on 18 May 2026. However, the analysis and financial metrics discussed here reflect the stock's current position as of 24 July 2026, providing investors with the latest insights into the company’s performance and outlook.

Read full news article

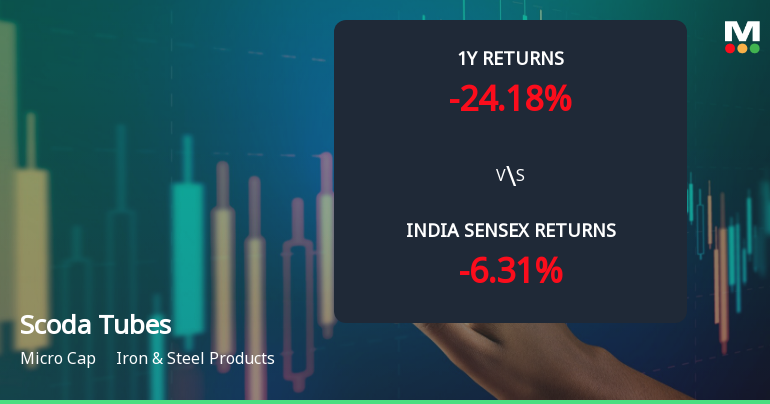

Scoda Tubes Ltd Technical Momentum Shifts Amid Bearish Sentiment

2026-07-17 08:02:51Scoda Tubes Ltd, a micro-cap player in the Iron & Steel Products sector, has experienced a notable shift in its technical momentum, moving from a sideways trend to a mildly bearish stance. Recent technical indicators reveal a complex picture, with mixed signals from MACD, RSI, moving averages, and other momentum oscillators, reflecting the stock’s struggle to regain upward momentum amid broader market pressures.

Read full news article

Scoda Tubes Ltd is Rated Sell

2026-07-13 10:10:17Scoda Tubes Ltd is rated 'Sell' by MarketsMOJO, with this rating last updated on 18 May 2026. However, the analysis and financial metrics discussed here reflect the company’s current position as of 13 July 2026, providing investors with the latest insights into its performance and outlook.

Read full news article

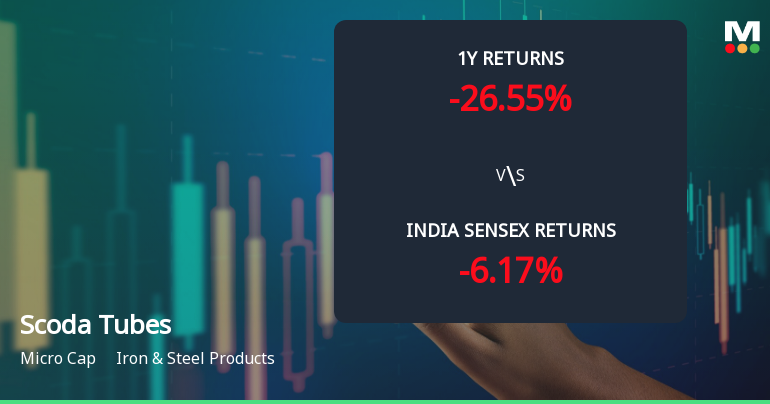

Scoda Tubes Ltd Technical Momentum Shifts Amid Mixed Market Signals

2026-07-08 08:06:40Scoda Tubes Ltd, a micro-cap player in the Iron & Steel Products sector, has experienced a notable shift in its technical momentum, moving from a mildly bearish stance to a sideways trend. Despite a recent downgrade from Hold to Sell by MarketsMOJO on 18 May 2026, the stock’s technical indicators present a complex picture, with some bullish signals emerging alongside persistent bearish pressures.

Read full news article

Scoda Tubes Ltd Technical Momentum Shifts Amid Mixed Market Signals

2026-07-07 08:08:38Scoda Tubes Ltd, a micro-cap player in the Iron & Steel Products sector, has experienced a notable shift in its technical momentum, reflecting a complex interplay of bullish and bearish signals across multiple timeframes. Despite a modest day gain of 0.27%, the stock’s technical indicators reveal a transition from sideways movement to a mildly bearish trend, prompting a downgrade in its Mojo Grade from Hold to Sell as of 18 May 2026.

Read full news article

Scoda Tubes Ltd is Rated Sell

2026-07-02 10:10:04Scoda Tubes Ltd is rated 'Sell' by MarketsMOJO, with this rating last updated on 18 May 2026. However, the analysis and financial metrics presented here reflect the stock's current position as of 02 July 2026, providing investors with the latest insights into the company’s performance and outlook.

Read full news article

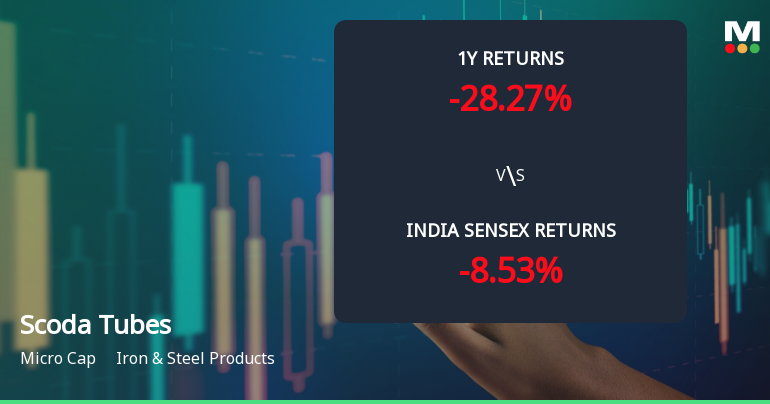

Scoda Tubes Ltd Technical Momentum Shifts Amid Mixed Market Signals

2026-07-01 08:05:54Scoda Tubes Ltd, a micro-cap player in the Iron & Steel Products sector, has experienced a notable shift in its technical momentum, moving from a mildly bearish stance to a sideways trend. Despite a modest day change of 0.03% with the stock price hovering at ₹143.35, the underlying technical indicators present a complex picture that investors must carefully analyse amid broader market dynamics.

Read full news articleCompliances-Certificate under Reg. 74 (5) of SEBI (DP) Regulations 2018

14-Jul-2026 | Source : BSECertificate under regulation 74(5) of SEBI (LODR) Regulations 2015 for the quarter ended on June 30 2026

Closure of Trading Window

25-Jun-2026 | Source : BSEClosure of Trading window w.e.f. Wednesday July 01 2026

Announcement under Regulation 30 (LODR)-Analyst / Investor Meet - Intimation

15-Jun-2026 | Source : BSEWith reference to the captioned subject and pursuant to Regulation 30 and Para A of Part A of Schedule III of the SEBI (Listing Obligations and Disclosure Requirements) Regulations 2015 we wish to inform you that company has schedule a plant visit for Group of Investors/Analysts at the registered office of the company situated at Survey Nos.: 2437 2442 2443 2446 Ahmedabad-Mehsana highway Village: Rajpur Tal. Kadi Dist. Mehsana Gujarat India 384440 on Friday June 19 2026.

Corporate Actions

No Upcoming Board Meetings

No Dividend history available

No Splits history available

No Bonus history available

No Rights history available