Reason #1: Albert Einstein’s Eighth wonder of the world

Albert Einstein called the Power of Compounding as the Eighth wonder of the world. HDFC Bank stock definitely fits that bill.

The stock has given a Compounded Annual return of 28% over the last 20 years. (The Sensex has given 13%).

Now let’s see the Magic of Compounding:

One lac invested in HDFC Bank in 1998 is now worth Rs.1.4 crore without considering the dividends. The same One lac in the Sensex would have given just 11.5 lacs.

Thus, HDFC Bank would have return 12.5x more than the BSE Sensex in the 20 years.

Eighth wonder of the world? Or Magic?

Reason#2: A First Among Equals

TCS recently became the first Indian company to touch a market cap of US$100 billion. Will HDFC Bank be the first Indian Bank to reach that milestone? With its current market cap of around Rs. 5,00,000 crores or US$75 billion, I would think so. The stock has all the necessary ingredients.

Let me put that in perspective. And the best way to do that would be to compare it to its banking peers.

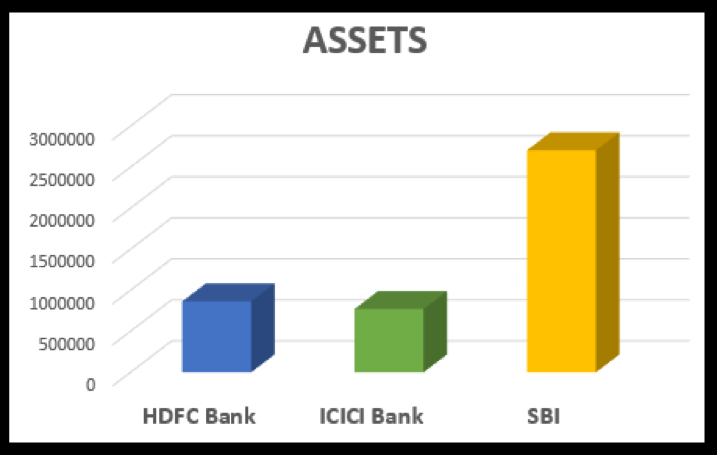

TOTAL ASSETS:

HDFC Bank and, ICICI Bank are almost neck-to-neck on the Total Assets. Both were founded in 1994. SBI which is bigger than both of them has a history which almost as old as the history of banking in India.

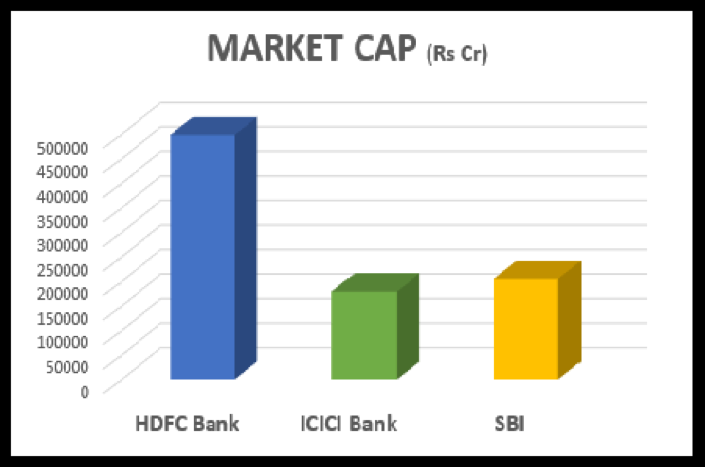

MARKET CAPITALISATION:

The market capitalization of HDFC Bank is more than that of ICICI Bank and SBI combined!

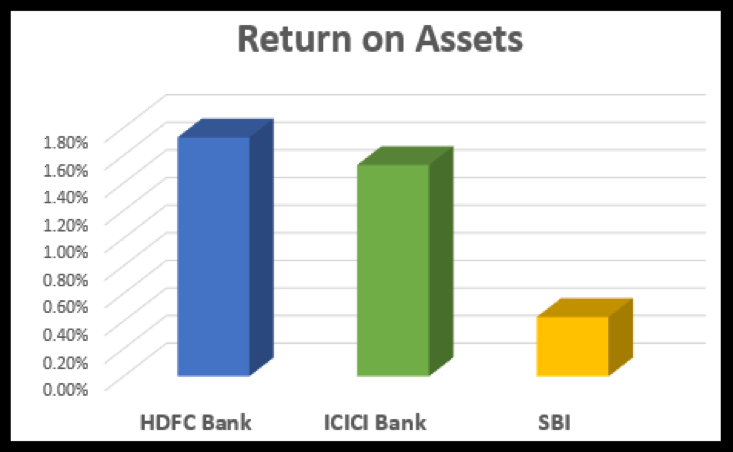

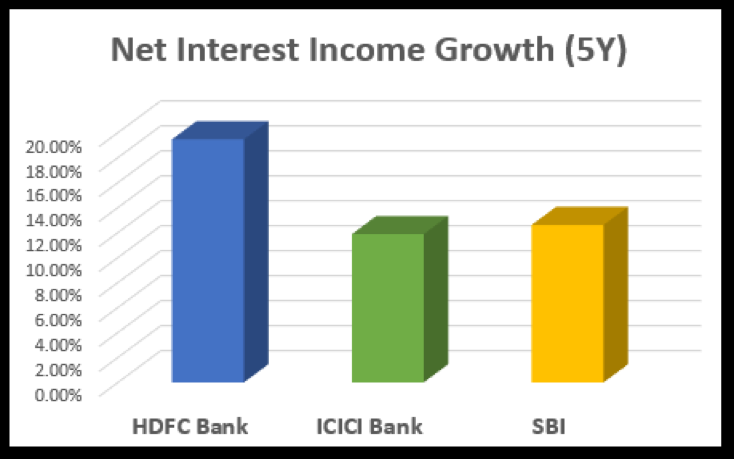

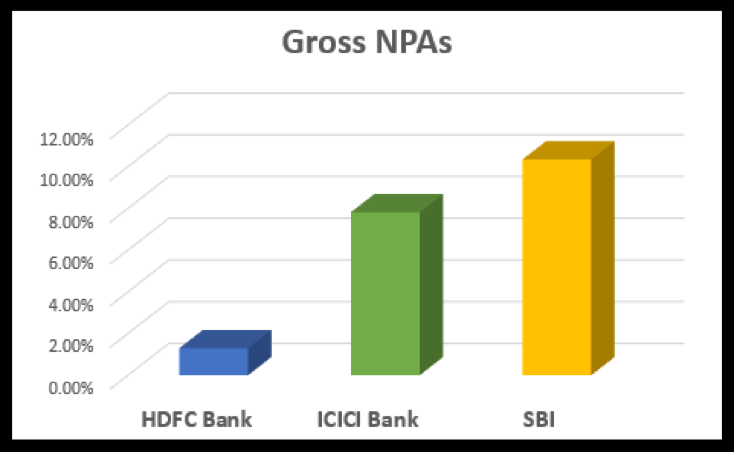

ROA, GROWTH, GROSS NPA:

The difference in these banks are highlighted in the three main parameters that one should evaluate banks on:

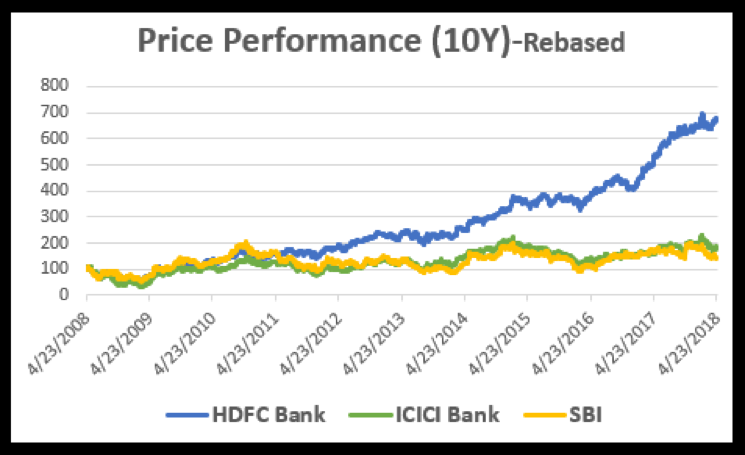

PRICE PERFORMANCE:

The price performance of the three banks in the last 10 years also tells the same story.

Notice how ICICI actually trades more like SBI than HDFC Bank!!

George Orwell would have said:

“All Banks are equal, but HDFC Bank is more equal than others.”

Reason #3: A classic Philip Fisher stock

Philip Fisher, one of legendary investors, had a very simple stock picking strategy:

“Purchase and hold for the long term a concentrated portfolio of outstanding companies with compelling growth prospects”

If there is one stock that fits this strategy perfectly, it is HDFC Bank.

The Bank is rated Excellent on our Mojo Quality parameter. In fact, it scores well on all the three Quality parameters of: Management Risk, Growth and Capital Structure. This can also be seen from its high ROA of 1.8%, Low Gross NPA of 1.3% and Five year net profit growth of 20%+.

Not only has the bank shown high growth, the growth prospects seem to be compelling as the India story unfolds and also it continues to gain market share from the Public-Sector Banks.

Motilal Oswal Securities in a recent report has articulated very well that HDFC Bank is ready to capitalize on the growth opportunities due to the following factors:

- CASA ratio of 43.5%,

- Opportunities’ for the significant market share gains

- Improving operating efficiency led by digitalization initiatives

- Expected traction in income due to strong expansion in branch network, and

- Best-in-class asset quality

Philip Fisher would have been delighted to hold HDFC Bank.

Reason # 4: The Bank deserves its high valuation

4.7X – that’s the Price to Book value of HDFC Bank.

This commonly used Valuation parameter for a bank seems very high. It has always been high, and that’s forever deterred many investors over the years.

In my earlier piece, Method in Madness I had said valuations of Banks depend on three legs:

- Profitability

- Risk

- Growth Prospects

Further, in another piece The 5 Best Banks to INVEST, I had demonstrated that the relationship of each of these variables with the valuation is non-linear.

Finally, the foregoing comparison with ICICI and SBI on the above parameters shows that HDFC Bank actually deserves the premium it commands.

We have taken into account all these factors and our Mojo Valuation parameter rates this Bank as Fair. The Motilal Oswal Securities report mentioned above gives a one year price target of Rs. 2400 to the Bank.

Reason # 5: The bank delivers quarter after quarter

- The Financial Trend has been positive every quarter since we started tracking 20 quarters ago

- HDFC Bank recently declared another quarter of stellar growth with Net profit growing 20% YoY in March 2018.

- HDFC Bank continues to register high profit growth while keeping its Non-Performing Assets (NPA) very low and very high return ratios.

- The Gross NPA based on March 2018 numbers is 1.3%. This is against close to 10% of Gross NPA of SBI reported in Dec 2017. The corresponding number for ICICI is around 8%.

- The ROA of HDFC Bank continues to be high at around 1.8% vs ICICI’s of 1.5% and SBI’s 0.4%

A stock which shows such high consistency gives less sleepless nights to the investors!

Who Should Hold such a stock?

HDFC Bank fits very well on all the four Mojo parameters

- The Quality is Excellent

- The Financial Trend Score is positive

- The Technicals continue to show a positive trend

- Despite the fantastic performance of the stock, Valuations are Fair

Overall HDFC Bank fits the portfolio both for near-term and long-term investors

The Beta of the stock at 0.79 is ideal for a long-term investors as lower volatility makes Buy & Hold strategy easier to implement.

Of course, a lower Beta is not great for shorter term traders, but HDFC Banks is rarely a stock for short term traders.

When to sell?

Philip Fisher famously said, “If the job has been correctly done when a stock is purchased, the time to sell it is — almost never.”

However, he did provide a framework for selling a stock. He says one should sell a stock if “the reasons you bought the stock are no longer valid”

This could happen mainly for the following two reasons “either there has been deterioration in the management quality of the company or the company cannot sustain the growth”.

If the growth tapers off, in a Philip Fisher stock, one gets enough time to sell as most participants in the market continue to believe that the growth will bounce back. Thus, we should worry only if the Financial Trend deteriorates for a few quarters in a row.

However, if the Management quality deteriorates, the risk is higher. In the case of HDFC Bank, the major driver of the bank has been its CEO Mr. Aditya Puri. Mr Puri is slated to retire in 2020. If the market perceives that the person who succeeds him is not capable, the stock will adjust. The good news is that there seems to be enough talent within the HDFC Group which means that this risk is not very high.

Let me know if you have a differing view or if you agree with Philip Fisher. Would love to hear what you think.

Sanjeev Mohta

Market Expert

Sanjeev Mohta is the Market Expert at Marketsmojo. He has over 27 years’ experience in Investment Research and Fund management across Asian Markets and Asset classes. He has worked in various organisations in Singapore and India like Alchemy, QVT, Jefferies, ABN Amro and HSBC Securities. He Has a PhD in Economics from Tulane University, USA.