While most of the financial analysts think linearly, the real world is anything but linear. One such non-linear phenomenon which creates multi-baggers is Operating Leverage.

Operating Leverage causes even a modest topline growth into a disproportionately high Bottomline growth. A continually high bottomline growth creates Multibaggers.

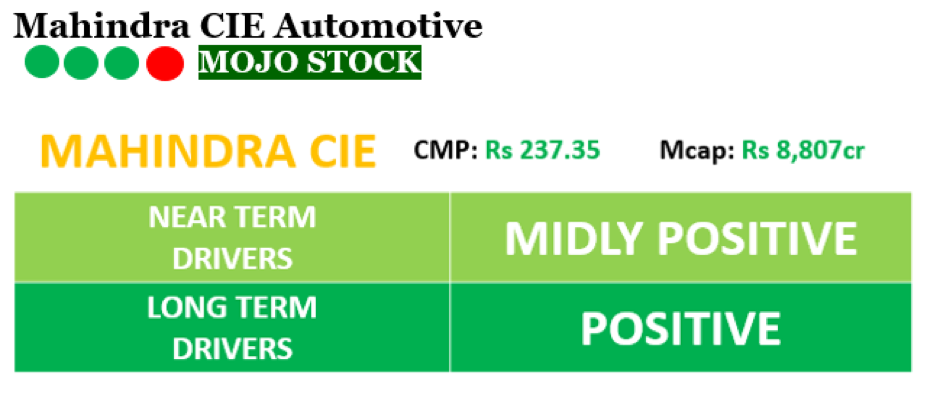

In this Marketsmojo Professional Exclusive, I have looked at the latest results of Mahindra CIE to explain this powerful concept of Operating Leverage.

Where 32% = 103%

The Growth in Sales and Gross Profit of Mahindra CIE in the quarter ended March 2018 vs March 2017 are both at 32%.

In a linear world, the profit should have grown by 32% as well. But, the Growth in Earnings before Interest and Taxes for this company is 102%.

This is Operating Leverage at work.

What is Operating Leverage?

Let me try and explain the concept of Operating Leverage in a very simple way.

A company’s Gross Profit measures its Value Addition. It is simply calculated by reducing the Raw Material Cost from Sales. Why? The business of a company, in general, is to take the Raw Materials and add value to it and sell.

If we subtract all the cost that goes into adding this value from the Gross Profit (GP), we get Earnings Before Interest and Tax (EBIT)

Assuming that these costs are not dependant on how much you sell. The Ratio of GP/EBIT gives what can be called Operating Leverage.

Let us calculate this for Mahindra CIE.

|

Just by Dividing the GP by EBIT we get Operating leverage. The Number was 7.7 in March 2017.

What this means is that if the GP grew at 10%, the EBIT should grow by 10% times 7.7 or 77% if other costs remain constant.

But other costs did not remain constant and grew by 22%. Hence whilst GP grew by 32%, the EBIT went up by 103%. Someone who would have done a linear analysis would have got it wrong.

Thus, we can see that the Operating Leverage plays a very big role in how much the bottom line grows by, given the top line growth.

So, what can one say about the future?

The current Operating Leverage is 5. Which means that the Operating Leverage for Mahindra CIE continues to be very high.

Simple Arithmetic shows that if the Gross Profit grows at 20% and if the Other Costs went up 10%, The EBIT can grow at 60%. You can do your own assumptions and calculations on this! If you think that the 30%+ growth is possible for some time, this stock could be a multi bagger.

A bit about Mahindra CIE

This Mid Cap company is an Alliance between the CIE group, Spain and the Mahindra Group, India; with the former holding the Majority stake.

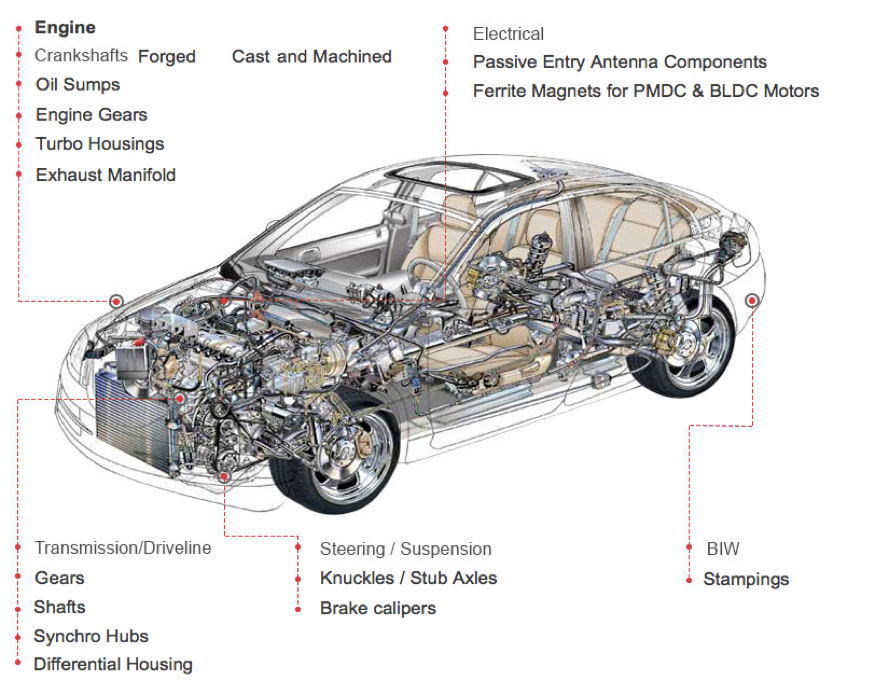

It is engaged in the manufacturing of world class forged and machined products for automotive, agriculture, railway, mining, construction and other industries. Some of what it does is shown below.

The company has a huge customer base that spans across the globe, you can find the list here.

The institutional holding of the company is at 13.3%, with 69.8% of the company held by its Promoters, and Non-Institutional holding is 16.8%

Over the last 5 years, the company has shown a Sales growth of 24.1%. In 2017, the Sales grew by 20%

The stock has underperformed over the last 1 year, and is up only 4.9%

Will the underperformance finally come to an end? Based on the above analysis that will depend on its growth in Gross Profit over the next few years.

How Operating Leverage creates multi-baggers

A company with high operating leverage can be a multi- bagger if it experiences a high growth in its Gross Profit. A good example of operating leverage in the recent past has been Philips Carbon Black. The table below shows this phenomenon in 3 simple numbers:

|

||||||||

Would love to hear your views on Mahindra CIE or any other stock which you think have high Operating Leverage. Please do write back to us at

support@marketsmojo.com

Sanjeev Mohta

Market Expert

Sanjeev Mohta is the Market Expert at Marketsmojo. He has over 27 years’ experience in Investment Research and Fund management across Asian Markets and Asset classes. He has worked in various organisations in Singapore and India like Alchemy, QVT, Jefferies, ABN Amro and HSBC Securities. He Has a PhD in Economics from Tulane University, USA.