After 13 years, one more company-Chalet Hotels-from the K Raheja group is going public with fresh issue of shares as well as offer for sale from promoters. The issue will open on 29th January and close on 31st January. The price band has been kept at Rs 275-280 per share. The company intends to raise Rs 1629 crore, of which Rs 950 crore would be fresh issue of capital, while the balance would be offer for sale.

I am a little surprised at the timing of the issue as well as the price the company expects from the investors. The sentiment in the market is very weak. On top of it, the company’s financials are also fluctuating. The company has reported loss for the first six months of the current financial year ending September 2018. That makes the possibility of investors making money on investment in the company’s issue a little low. In all probability, Chalet Hotels may not turn out to be a wealth creator for the investors.

Inter-related party transactions

Chalet Hotels owns hotels. It buys land and constructs hotels on the same. K Raheja group has many business verticals like retail, residential, commercial and hotels. For each business vertical, the group requires land. I am not sure how the group can ensure that land would be available at reasonable price for the listed entity-Chalet. When asked, the management said that, in the past, as and when land was acquired from the group companies, it was acquired at cost-plus basis. This creates some kind of issues on transparency. In the recent past, we have seen that the share price takes a huge beating even when there is a small doubt on corporate governance. In that sense, I have a feeling that Chalet may not command the premium which otherwise it would have commanded had there been fewer related party transactions.

Shoppers Stop-Another group company did not create that wow moment for investors

In 2005, when Shoppers Stop came out with an IPO, it gave hope to the investors that this company would create wealth for them as the retail industry then looked promising. But that was not to be. It made an IPO at Rs 238 (face value Rs 10) against which the price is at Rs 517 (FV Rs 5). It gave CAGR of 11 per cent since listing. I would say that this is an average return as the company had the first mover advantage, but it failed to capitalise on the same. Sensex during the same period gave much better returns of 13 per cent CAGR. Its present market cap is Rs 4,500 crore. In the last five years, Shoppers Stop underperformed the broader market as the share price has gone up by 36 per cent, while Sensex during the same period is up by 72 per cent. This despite retail being the flavour of the season. Players like Avenue Supermarts (D-Mart) did extremely well in the retail business and enjoys market cap of Rs 85,000 crore. K Raheja group had Hypercity in its portfolio (where Shoppers Stop also had a stake), a business that can be compared with D-Mart, but it could not scale up and ultimately sold out to the Future group. Just for comparison, Future Retail has a market cap of Rs 22,000 crore. That gives me a feeling that the group is not able to scale up business and that is a risk Chalet Hotels may also carry.

Its Vashi hotel is under litigation

The company operates Four Points by Sheraton Hotel at Vashi. This was purchased from promoter K Raheja in December 2005. Due to two PILs, the Mumbai High Court during FY14-15 directed K Raheja to demolish the hotel and give it back to CIDCO. The company filed special leave petition against the order in the Supreme Court and the apex court has ordered maintaining the status quo till the court announces final verdict. In case the ruling goes against the company, it can adversely impact the sentiments as well as the financials of the company.

Hotel industry did not create wealth for the investors

The stocks of hotel companies have struggled to create wealth for the investors. This shows that they are not the darling of the investors. In the last one year almost, the stocks of all hotel companies have underperformed the broader market. There is a reason for the same. The industry saw excess supply of room inventories and, due to that, the occupancy rates as well as ADR (average daily rate) took a beating. In the recent past, there has been uptick in the room rates and occupancy rates, but it is a little early to call it a trend. Also, this industry is facing challenges from new start-ups like Airbnb and OYO. Despite OYO being in the budget segment (Chalet is in the premium segment), it does impact demand. I am not sure whether the hotel industry is on the cusp of rerating. Many hotel properties today are available below their replacement cost, thereby reflecting poor sentiment for the sector.

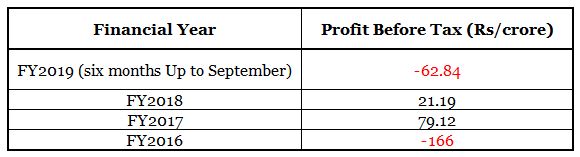

Volatile Financials

The company’s financials are not of much comfort to the investors. For FY2016, the company’s loss at PBT level (before exceptional items) was Rs 166 crore. The same figure improved in FY2017, where the company reported profit of Rs 79.12 crore. But again, it took a dip in FY2018, when the profit declined to Rs 21.19 crore. In the first six months of the current year, the PBT (before exceptional items) showed a loss of Rs 62.84 crore. In all probability, the company will report losses in the current financial year. The past financial performance does not inspire much confidence.

Valuations

Despite the volatile financials, the company wants rich premium from investors. Based on the price band, the company will command market cap of Rs 5,655 crore. Indian Hotels (Taj group of hotels) commands market cap of Rs 16,000 crore, while EIH Ltd (Oberoi group of hotels) commands market cap of Rs 10,000 crore. Based on March 2018 numbers, the company would command EV/EBDIT of 24 times, which is equivalent to what Indian Hotels is commanding. For the first six months, the company’s financials have deteriorated and hence EV/EBDIT has further moved into expensive territory. This does not leave scope for capital appreciation.

In all probability, Chalet Hotels will not live up to the investors’ expectations. I would not be subscribing to the IPO.

Sunil Damania

@sunildamania

Disclaimer: This blog is only for education purpose. We don’t give buy or sell call on any company. All investors are advised to do their independent research and/or consult their financial advisor.

Sunil Damania

Chief Investment Officer - Marketsmojo.com

A chartered accountant, has 25 years of rich experience tracking Indian as well global stock markets. He has a strong command over financial analysis and an in-depth understanding of the stock market. He has been a speaker at various events such as Funds world India, Tradetech India, Assocham to name a few. His excellent application of common sense helps him find true gems in the equity market to create alpha.