“In the short run, the market is a voting machine but in the long run it is a weighing machine” Benjamin Graham

Valuation is a long-term driver for stock market returns. In the short term the markets can become very expensive or very cheap depending on the overall sentiment and news-flow. However, over the longer-term Valuation plays an important role in determining the return as market takes into account not only the growth but also what price has been paid for it.

In this Marketsmojo Professional Exclusive I look at the current Valuation of the overall market and try to decipher what that means for us as investors.

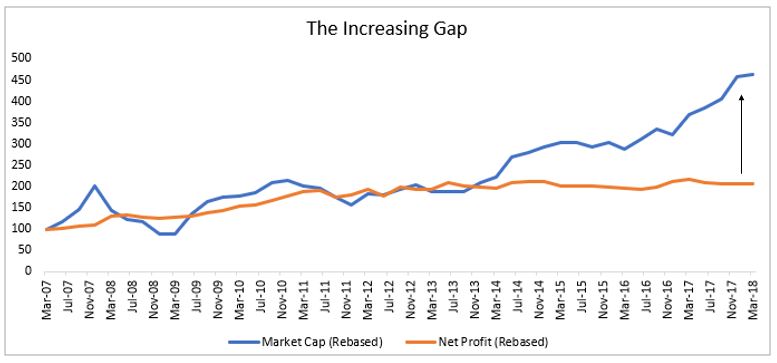

The Market has been going up but the Earnings have not kept pace

Over the long-term stock prices move with the earnings. In the interim, there can be divergences. We are passing through such a stage since the beginning of 2014. The chart below clearly shows that the Market Cap of India Inc. has gone up without commensurate increase in Earnings.

The profits have shown a negative growth in second half of FY 2016 and the first half of FY 2017. Over the last few quarters the profit has grown but has only caught up with the profits in FY 2015.

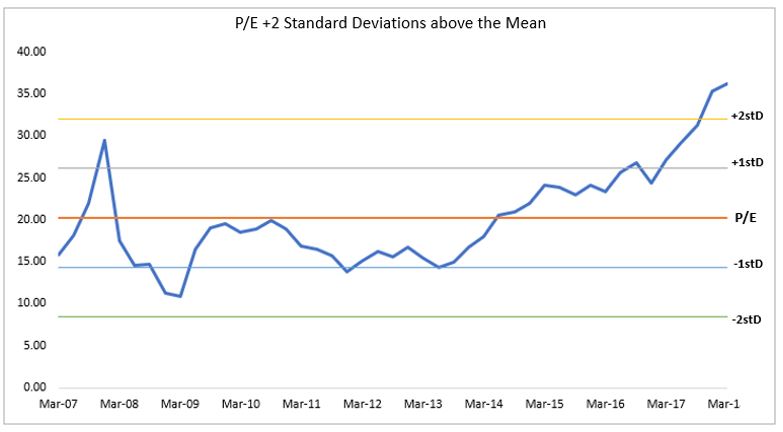

Thus, P/E Ratio has gone up a lot

This profit stagnation coupled with the rise in stock prices has led to a rise in the Price/Earnings (P?E) ratio of the market. The Market Cap weighted P/E ratio of all the listed companies put together is around 35x on past earnings. This is definitely not cheap.

In Fact the P/E is More than 2 Standard Deviations from the Mean

The chart below shows that the P/E ratio, in fact, is more that 2 standard deviations higher than the mean since 2007.

The Average P/E of the Indian market since 2007 is around 21x its historical earnings. The current valuation of more than 35x is close to its highest level over the last 11 years. Based on P/E ratio, one can say that either the market is highly overvalued or that the market is expecting the earnings to catch up pretty fast. In effect it is expecting a very high earnings growth over the next couple of years. Does this mean that we are in an Euphoria stage

It does not imply, though, that we are in Euphoria

In my piece, The Four Phases of a Bull Market, I had written about the phases of a Bull market. The idea was based on the famous quote by Sir John Templeton: “Bull markets are born on pessimism, grown on scepticism, mature on optimism, and die on euphoria.” One of the key features of Euphoria phase is that the valuations are very high. Based on P/E this seems to be so.

Mr Jeremey Grantham, a market legend and one of the most influential voices in the investment world, is particularly noted for his prediction of various bubbles. He says that an important indicator for Euphoria is that the overall fundamentals have to be positive and the market is extrapolating these fundamentals to go on forever. However, as noted above, this high P/E is accompanied by close to zero growth of profits. To that extent the overall fundamentals are not yet positive. So despite the high valuation this stage cannot be described as Euphoric. For Euphoria to happen we should be in a phase which has seen high earnings growth along with high P/E.

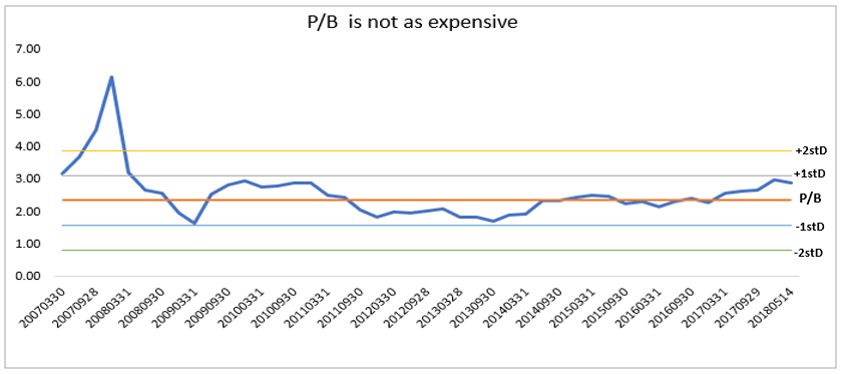

Valuations based on Price/Book are less extreme

I believe that Price/Book (P/B) is a much better measure of valuation than P/E, at least for the overall market. One good feature of P/B is that can be compared across Financial and Non-Financial sectors. Also Book Value, or any other Balance Sheet factor like Capital Employed, is far more stable than Earnings and hence P/B is much less volatile compared to P/E. P/E, for example, can seem very high when earnings are low.

The chart below shows that P/B at 2.9x is higher than the long term mean, but it is within one standard deviation from the mean.

The absolute P/B of around 2.9x is still not cheap especially as the Return on Equity of India’s corporate sector has come down due to stagnant earnings. However, it is nowhere near the Extremely overvalued zone.

What are the implications for us, as Investors?

The above analysis implies that while not Euphoric, the market is definitely not cheap. As investors, we need to be mindful of the following:

- The high P/E is implying that the market is expecting the growth to soon accelerate. If that does not happen market will not be able to sustain these levels. We need to keep a close watch on the Earnings growth. Thankfully the corporate earnings seem to have turned around from its bottom in the last few quarters, but will this continue?

- Higher than Average Valuation means lower than average returns. For example, if you bought the BSE500 at the peak P/B of almost 6x in December 2007, the return till date is a low 5.5% per year. However, if you bought the BSE500 at the low P/B of around 1.66x in March 2009, the return would have been a CAGR of 17%. Last time we saw a valuation of 2.9x was in December 2010. Since then the market has given a return of 13.5% CAGR.

- When the Valuations are high, the ability to absorb bad news becomes less. Using Benjamin Graham’s terminology, the Margin for Safety in the Market is low. This also means that in a period when news is unpredictable the volatility in the market can be high.

- Bottom Up stock picking should do better. The averages most of the time hide more than they reveal. Even in sideways markets there are always individual stocks that can do very well. In a market that is expected to give slightly less than average returns, it is worth focussing on individual stocks or funds who have a great long-term track record of picking stocks.

Would love to hear your views/ feedback.

Sanjeev Mohta

Market Expert

Sanjeev Mohta is the Market Expert at Marketsmojo. He has over 27 years’ experience in Investment Research and Fund management across Asian Markets and Asset classes. He has worked in various organisations in Singapore and India like Alchemy, QVT, Jefferies, ABN Amro and HSBC Securities. He Has a PhD in Economics from Tulane University, USA.