Why the Two-Wheeler Industry?

Two-wheeler industry in India is one of the largest in the world with sales of more than Two crore vehicles in 2017-18. The Top 4 listed two-wheeler companies: Bajaj Auto, Eicher Motors, Hero MotoCorp and TVS Motor Company are all large Cap companies with well-known brands. To be fair Eicher Motors also makes commercial vehicles and Bajaj Auto makes Three Wheelers. However, Two Wheelers are the main drivers of their stock price performances.

The Two-Wheeler sector has been growing steadily over the last few years on India’s rising income and growing middle class. The demographics in India with probably the largest young population in the world also helps. These are long term secular themes. Add to this the growth may receive a further fillip as it is also a beneficiary of the Rural story.

How to find the Best Long-Term Pick?

Based on the analysis of millions of data points we have found that companies with good Quality and reasonable Valuation have beaten the market performance over the longer term. This ties in well with the strategies of most of legendary long-term investors. Our company Dashboard presents the analysis of these long-term drivers for each company.

Long Term Driver # 1: Quality

The business model of the Top Four listed Two-wheeler companies is very robust as they are Asset light, highly cash generative companies with very strong balance-sheet. Only TVS Motors has debt in their books, but even that is at very manageable levels. Some of the key parameters that go into our analysis of Quality capture this well:

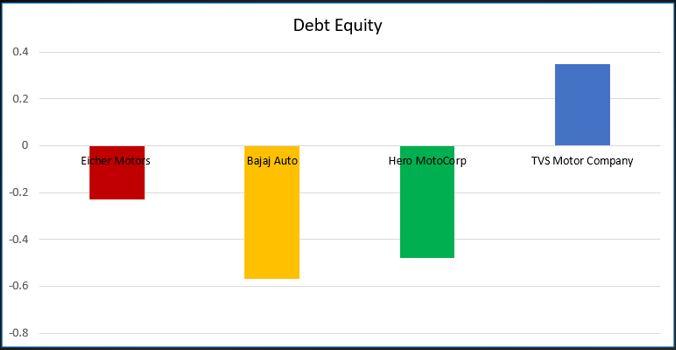

Balance Sheet

The Balance sheets of these companies are extremely strong. Other than TVS Motors none of them have debt. The Negative Net Debt to Equity implies that they have surplus cash/ investments in their balance sheet. In businesses that do not regularly raise money from external investors this is a clear indicator that these businesses are highly cash generative.

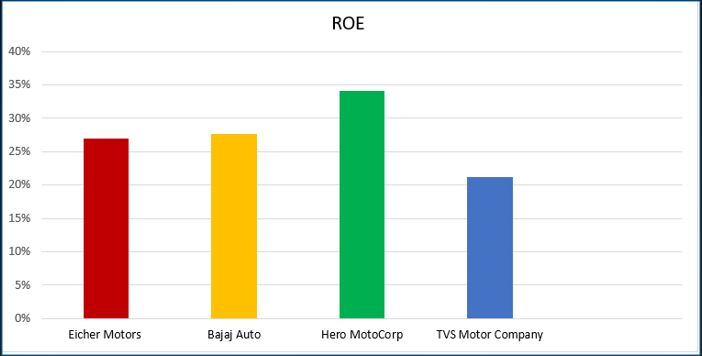

The Profitability

The best measure of profitability for companies that have no debt is the Return on Equity (ROE). To smooth out impact of business cycles it is good to look at 5 year averages. A 12-15% ROE is considered a reasonable return on the Equity that a company has. These companies have average 5 year ROE which higher than 20%. This helps them fund future expansions and any extra working capital needs without raising fresh capital or borrowing. This ties in well with the Negative Debt that we saw earlier.

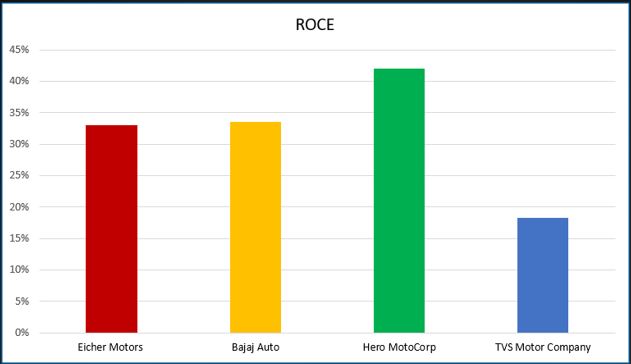

The Return on Capital Employed (ROCE) is a better measure than ROE for companies with debt. However, it still instructive to look at this number. The 5 year average ROCE of the three is higher than ROE again confirming the analysis of ROE. TVS Motor’s ROCE is however a bit lower because of the Debt that it has on its balance sheet but it is still above 15%.

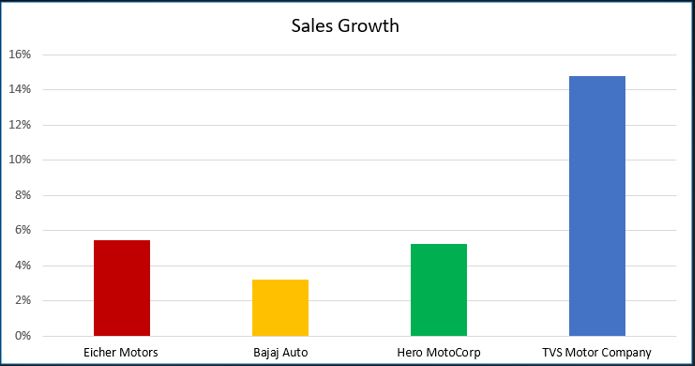

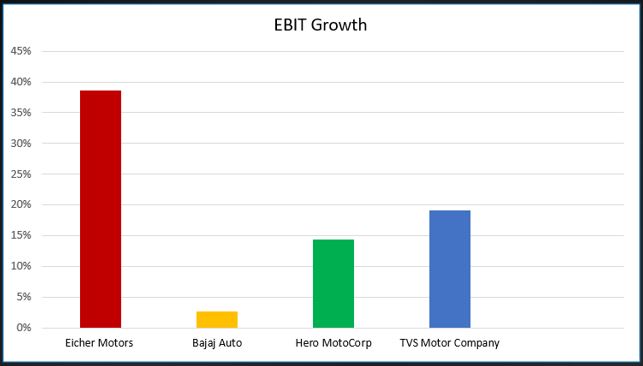

Past Growth

The average 5-year sales growth has been high for TVS Motor. However, the growth for others is not too high. Bajaj Auto has been especially disappointing. This partly reflects the consolidation phase in the Indian economy and the fact that this sector is reasonably mature.

The EBIT growth, other than for Bajaj Auto, has been higher than the Sales growth indicating that the margins have improved for the other three. The growth in Eicher Motors has been much higher partly as it morphed into mainly a two-wheeler company.

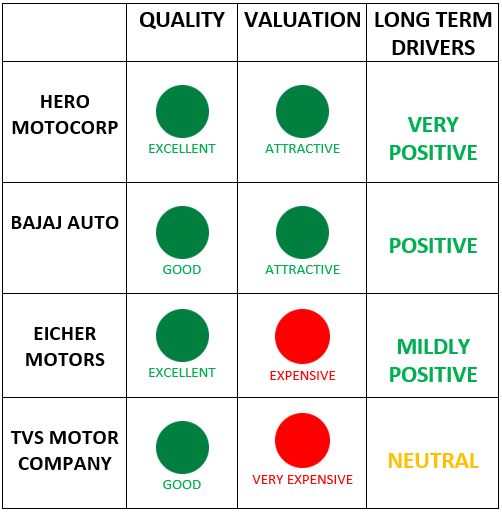

Overall, based on these and some more parameters, our prognosis is that Hero MotoCorp and Eicher Motors quality as Excellent Quality stocks which Bajaj Auto and TVS Motor Company qualify as Good Quality stocks.

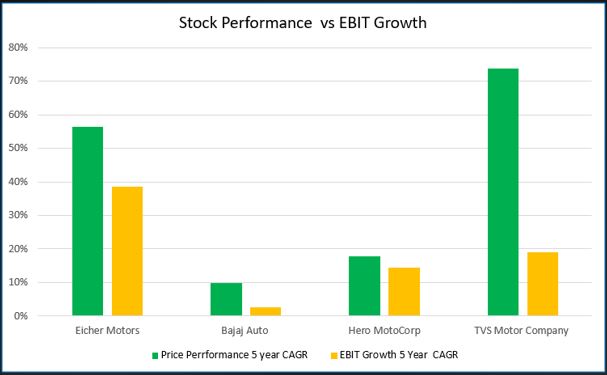

5-year Price Performance

It is interesting to see how the stock price movement has been for each stock relative to the EBIT growth.

Notice the following:

- The price performance of each stock has been higher than the EBIT growth, to some extent reflecting the bullish markets overall.

- The EBIT growth has played a role in determining the extent of price performance.

- In the case of TVS Motor, the divergence between price performance and EBIT growth has been extremely high.

- Eicher Motors has also shown something similar although to a lesser extent.

This analysis is a perfect prelude to our next Driver.

Long Term Driver # 2: Valuation

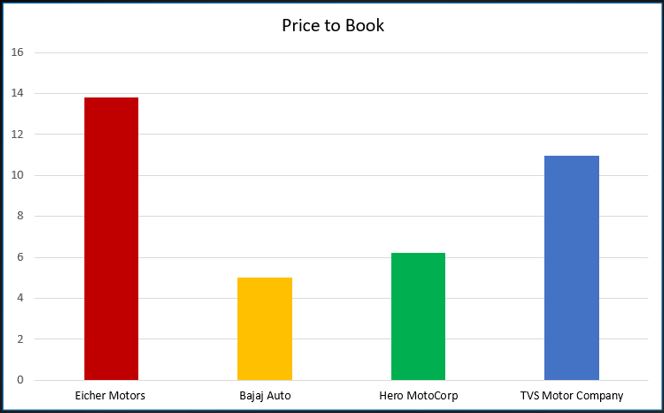

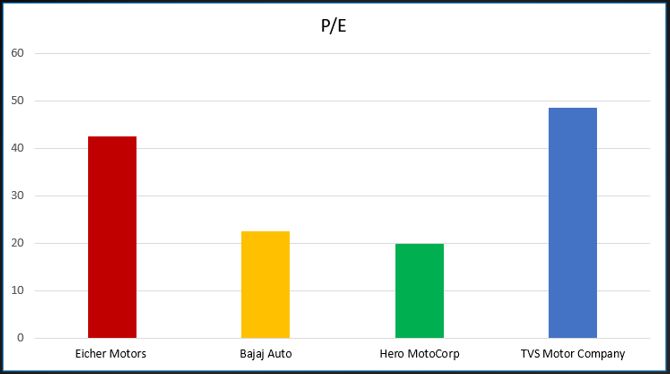

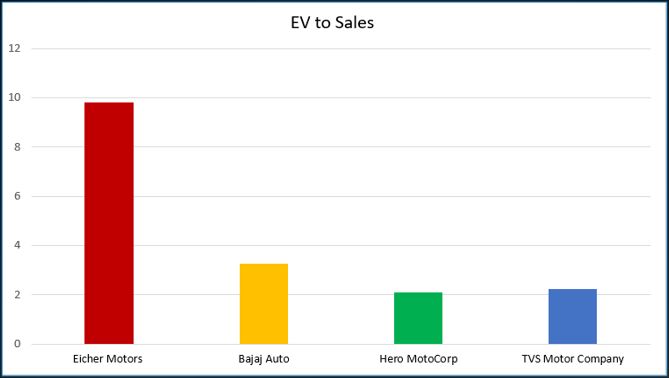

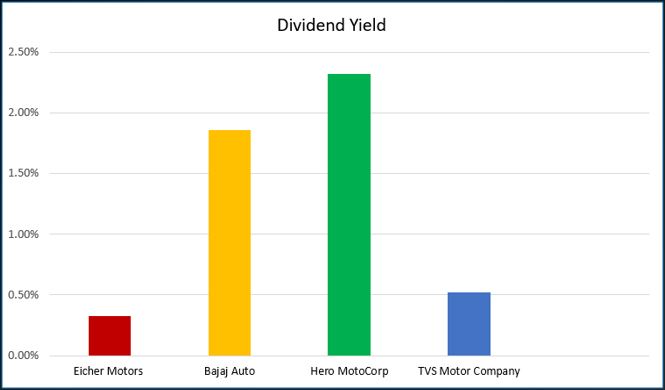

One of the best measures of Valuation of debt free companies is the Price to Book Value (P/B). Given that the Book value is a Balance Sheet measure, it is much less volatile than any earnings based valuation like P/E. However, we also look at measures like Price Earnings Ratio (P/E), Enterprise Value (EV) to Sales and Dividend Yield to assess the Valuation of these companies.

While the above charts very clearly tell a perfect story, to analyse the valuation we also put these numbers in the context of Balance Sheet, Profitability and Growth.

Based on our analysis, TVS Motor Company and Eicher Motors come out as Very Expensive or Expensive on every Valuation parameter.

Here is the summary of the Long-Term Drivers:

Based on the above, Hero MotoCorp, with Very Positive, stands out as having the best drivers of Long-Term stock performance in place.

What about the Beta?

In my piece, Stocks that spell danger for Buy and Hold Investors, I had pointed out that High Beta stocks create difficulties in Buy and Hold Portfolios. So, it may be a good idea to check that first.

| Beta | |

| Hero MotoCorp | 0.82 |

| Bajaj Auto | 1.02 |

| Eicher Motors | 0.72 |

| TVS Motor Company | 1.06 |

The Beta for all four stocks is not very high but Eicher Motors and Hero MotoCorp stand out.

I would not put a low Beta as a necessary condition to consider a stock for Buy & Hold, especially if all other factors are perfect, but the low Beta does help and Hero MotoCorp’s beta fits the bill.

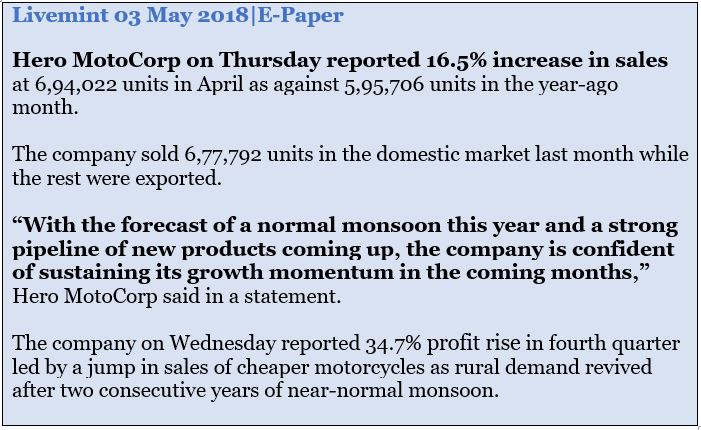

How has the recent Newsflow been?

A look at the news section on our site or a simple Google search on Hero Motocorp News can give lot of information.

For example, here’s the latest news on the company and this is positive as well.

What are the Brokers saying?

Given that these are all large cap many brokers cover these stocks. In a recent report Kotak Securities has a one year price target of Rs. 4353 on the stock which is a potential return of 19%.

Again, a broker report is not necessary but it helps.

To sum it all up

Given the analysis above one can conclude that Hero MotoCorp is a stock worth considering for Long Term investors.

Also, these kind of Large Cap stocks with Excellent Quality, High ROE, Solid Balance Sheet and reasonable valuations especially help during uncertain times.

With a spate of state elections culminating into the General Elections in 2019 and global policy uncertainty it’s better to bullet proof part of your portfolio!

Sanjeev Mohta

Market Expert

Sanjeev Mohta is the Market Expert at Marketsmojo. He has over 27 years’ experience in Investment Research and Fund management across Asian Markets and Asset classes. He has worked in various organisations in Singapore and India like Alchemy, QVT, Jefferies, ABN Amro and HSBC Securities. He Has a PhD in Economics from Tulane University, USA.