Yesterday’s ET story says,“Warren Buffett in Talks for a Slice of Paytm”.

Let’s discuss how Warren Buffett finds a great business.

His 2007 newsletter reads: “A truly great business must have an enduring ‘moat’ that protects excellent returns on invested capital (ROIC).”

At Marketsmojo we use the concept of Return on Capital Employed (ROCE) to uncover great companies that can deliver fantastic shareholder returns.

In this, the fourth piece in the series of Going to Bed Smarter, I present pieces which let you into the secret of ROCE.

The Magic of ROCE

The 2007 letter of Berkshire Hathaway is a classic. If there is only one Berkshire Hathaway letter you want to read, this one is it. In that letter, Warren Buffett narrates the success of See’s Candy.

“We bought See’s for $25 million when its sales were $30 million and pre-tax earnings were less than $5 million. The capital then required to conduct the business was $8 million (Modest seasonal debt was also needed for a few months each year). Consequently, the company was earning 60% pre-tax on invested capital. Two factors helped to minimize the funds required for operations. First, the product was sold for cash, and that eliminated accounts receivable. Second, the production and distribution cycle was short, which minimized inventories.

Last year See’s sales were $383 million, and pre-tax profits were $82 million. The capital now required to run the business is $40 million. This means we have had to reinvest only $32 million since 1972 to handle the modest physical growth – and somewhat immodest financial growth – of the business. In the meantime pre-tax earnings have totaled $1.35 billion. All of that, except for the $32 million, has been sent to Berkshire (or, in the early years, to Blue Chip). After paying corporate taxes on the profits, we have used the rest to buy other attractive businesses. Just as Adam and Eve kick-started an activity that led to six billion humans, See’s has given birth to multiple new streams of cash for us. (The biblical command to “be fruitful and multiply” is one we take seriously at Berkshire.)

There aren’t many See’s in Corporate America. Typically, companies that increase their earnings from $5 million to $82 million require, say, $400 million or so of capital investment to finance their growth. That’s because growing businesses have both working capital needs that increase in proportion to sales growth and significant requirements for fixed asset investments.

A company that needs large increases in capital to engender its growth may well prove to be a satisfactory investment. There is, to follow through on our example, nothing shabby about earning $82 million pre-tax on $400 million of net tangible assets. But that equation for the owner is vastly different from the See’s situation. It’s far better to have an ever-increasing stream of earnings with virtually no major capital requirements. Ask Microsoft or Google.”

ROCE = EBIT/Capital Employed

How do we calculated ROCE? Well, there are a few variants. But the easiest one is shown in this paper by Mirae Asset Management. Marketsmojo uses the same method.

EBIT is easy to calculate, but what about the Capital Employed? The paper says: “Capital Employed is the capital investment necessary for a business to function. It is commonly represented as total assets less current liabilities (or Fixed Assets plus Working Capital).”

ROCE is a far more useful measure compared to Return on Equity (ROE) as: “ ROCE is especially useful when comparing the performance of companies in capital-intensive sectors such as utilities and telecoms. This is because unlike return on equity (ROE), which only analyzes profitability related to a company’s equity, ROCE considers debt and other liabilities as well. This provides a better indication of financial performance for companies with significant debt.”

It follows from the equation that in order to generate high ROCE, a company must either have very high profit margins or need low levels of Capital Employed or a combination of the two.

We have had many such companies in India as well. Many consumer related business enjoy high ROCE due to their Asset Light nature. Hindustan Unilever with ROCE at close to 800%, Nestle at 400%, Page Industries at 84% are great examples.

High ROCE Means High Valuation

In 1997, when running research for HSBC, I had written a piece on the importance of ROCE. I had found that, everything else remaining the same, high ROCE companies enjoy far higher valuation that companies with low ROCE. At least for the companies where market believes that the high ROCE is sustainable.

A 2011 report, “Impact of ROCE on valuation”, by PWC concluded: “Companies that deliver better Return on Capital Employed (ROCE) experience higher valuation”

The relationship remains the same today. Is it any wonder why Hindustan Unilever, Nestle or Page Industries enjoy such high valuations?

At Marketsmojo, the five-year average ROCE is one of the most important metric used in our Quality Parameter.

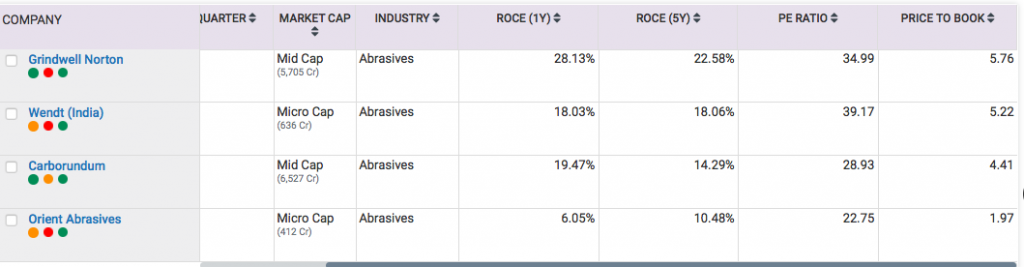

An interesting example: The Abrasives Industry

Let us look at the Abrasives Industry (which was picked randomly) which has a fairly uniform product, the relationship between the five-year average ROCE and Price/Book Value is fairly consistent with the findings above.

Next time you look at a stock, don’t forget to look at its long term ROCE – it’ll give you an insight about the inherent strength of the company’s business, and its ability to squeeze value from every rupee of capital. That will not only determine its valuation but also the price performance.

Also Read:

Going to Bed Smarter #1: Selling Too Early

Sanjeev Mohta

Market Expert

Sanjeev Mohta is the Market Expert at Marketsmojo. He has over 27 years’ experience in Investment Research and Fund management across Asian Markets and Asset classes. He has worked in various organisations in Singapore and India like Alchemy, QVT, Jefferies, ABN Amro and HSBC Securities. He Has a PhD in Economics from Tulane University, USA.