Last night I watched another Royal Challengers Bangalore (RCB) game against the SunRisers Hyderabad hoping to finally see the magic of Virat Kohli and AB de Villiers unfold. Unfortunately, another disappointment. They are all but out of the 2018 IPL.

Somehow RCB has just not lived up to its potential ever since IPL started ten years ago. Sure, they have finished second three times. But they are one of the few teams of the current lot never to win the IPL.

The story of ICICI Bank, which announced its eighth consecutive poor quarterly results yesterday almost seems like that of RCB. Like RCB they always have looked great on paper but have not delivered what was expected of them.

Opportunities Missed

The IPL started in 2008, just before the Global Financial Crisis. It is interesting that 2008 became a turning point for banking across the world.

While the stock markets collapsed everywhere, but the banking crisis was more a phenomenon of the Western Banks. This made most of the global banks look inward. The Local (country specific) Banks got a huge opportunity. Especially in Asia, the banks that were not fundamentally impacted by the crisis got an opportunity to become much bigger. In India, you had the added phenomenon of the problems with the PSU Banks. The Private sector Banks have had an open field.

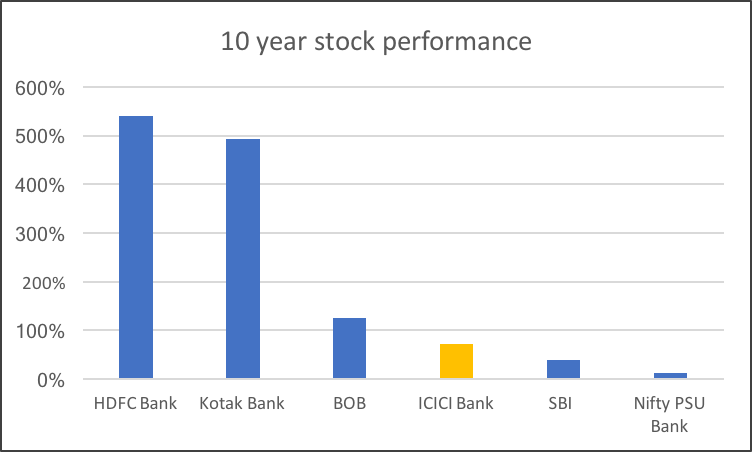

HDFC Bank and some of the other private sector banks like Kotak Mah. Bank, IndusInd Bank etc. have made the most of this. HDFC Bank’s market cap now is almost 3 times that of Deutsche Bank. ICICI Bank should have been a huge beneficiary but they seem to have missed out most of the opportunity at least so far.

Its 10 years since the crisis and the 10-year stock performance tells this story of missed opportunity very well.

The ICICI Bank stock has behaved more like its PSU counterparts rather than the other Private sector Banks.

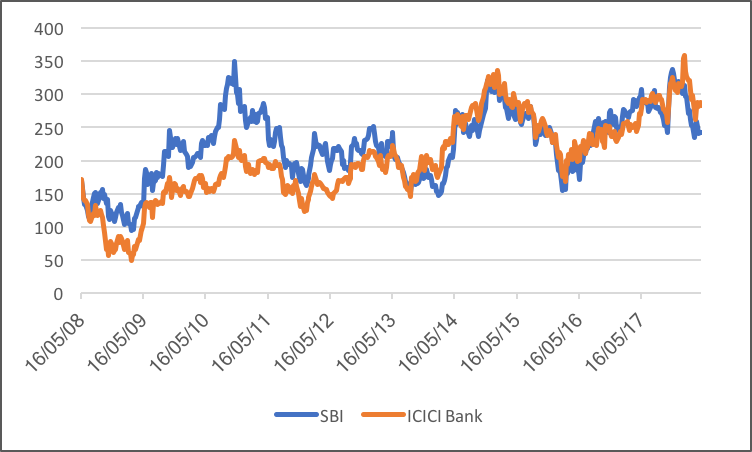

The weekly stock price performance relative to SBI is uncanny!

All the important ratios confirm the story as well.

- The ROA at around 0.87% is less than half that of HDFC Bank

- The GNPA of more than 8% is more like the PSU Banks.

- Net Profits have not grown over the last 5 years.

The recent News-flow on their CEO Chanda Kochhar has not helped either.

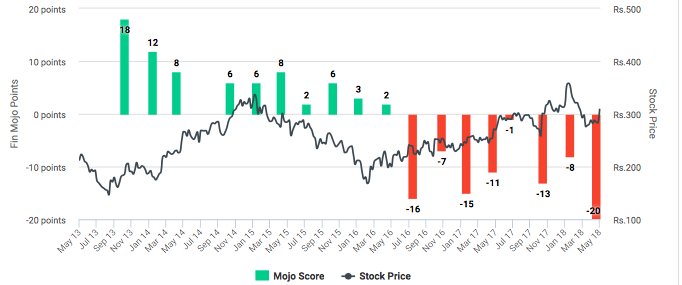

The latest results are more of the same

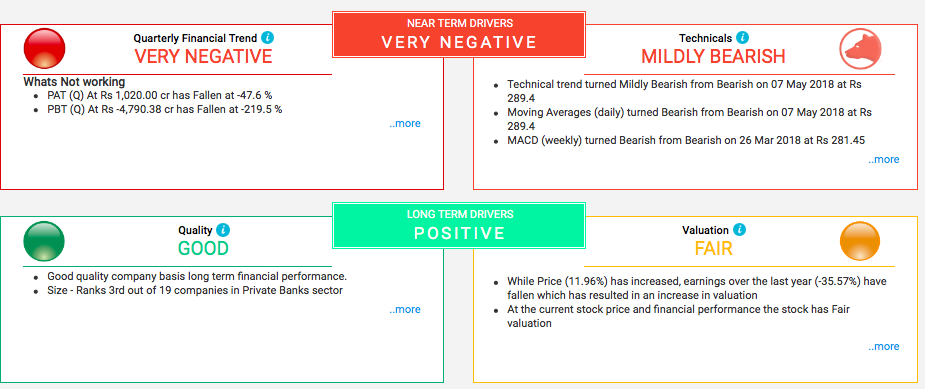

ICICI has just announced very poor results. On the Mojo Financial Trend Score they score a Negative 20. As already mentioned, this was the 8th consecutive bad result from the bank, but this score is the lowest so far, based on our analysis.

In fact, if one takes out the gain from the sale of shares of ICICI Securities for the IPO the company would have reported a loss for the Quarter.

Amongst all this gloom there are some Positives

- They do have a great brand. According to an analysis done by Hindu Business line in November 2017, ICICI is one of the top 10 brands in India. You may love or hate ICICI Bank, but it is difficult to argue against that.

- ICICI Bank is almost 90% owned by various institutions. The list is very broad-based. FII’s own 48% of the bank. To that extent the organization is much bigger than any individual.

- Based on our Analysis the Valuation comes out as Fair. The Price/Book of the Bank is around 1.8x.

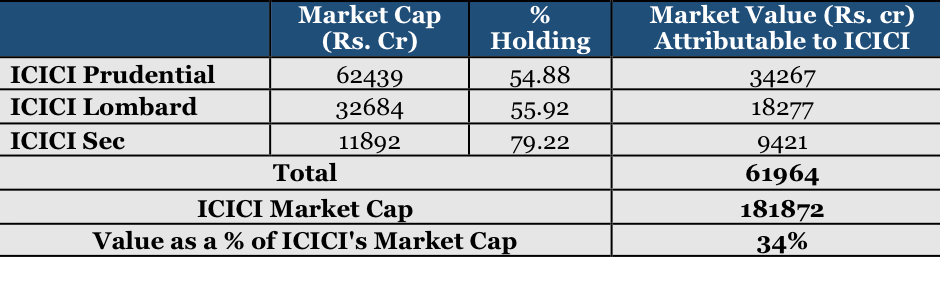

- The subsidiaries are very valuable. For example, a look at the Market Value of the listed subsidiaries shows that one third of ICICI’s market cap can be attributable to them.

Is the worst over?

There were two statements in the post results statement released by ICICI which makes one slightly positive:

- Provision coverage ratio increased by 690 bps from 53.6% at March 31, 2017 to 60.5% at March 31, 2018. The increase in coverage makes the numbers less aggressive.

- The Bank’s below investment grade exposure in key sectors identified earlier and promoter entities decreased from Rs 44,065 crore at March 31, 2016 to Rs.4,728 crore at March 31, 2018. Hopefully this means that the chances of a blowout in NPA numbers in the future has reduced.

Also, the good news for the stock is that after falling to a recent low of Rs 256 it has bounced back more than 15%. The post results price reaction has been positive, which probably means that the current bad news is in the price. The stock is close to where it was at the beginning of the year.

If things go right the upside can be good and it will also be helped by the fact that valuation is a non-linear function of the underlying performance (for example ROA). I had showed the relationship in an earlier piece. So, investors can potentially gain from underlying growth and an improvement in valuation

But when? While the long term drivers are fine, the short-term drivers continue to be negative for the stock.

Also, even if the worst is over for the bank it is not easy to predict when the good times will return. Given that the bank has had a history of missing opportunities it may be prudent to wait and watch

We have seen over the last few weeks how badly RCB can play, certainly it cannot get worse than this. For all you know RCB will finally play to its potential and win the IPL in 2019. Who knows 2019 may also be the year for ICICI.

My personal view is that one should definitely put the stock in the watch list and track the financial performance regularly to see if things are improving.

Would love to hear your views.

Sanjeev Mohta

Market Expert

Sanjeev Mohta is the Market Expert at Marketsmojo. He has over 27 years’ experience in Investment Research and Fund management across Asian Markets and Asset classes. He has worked in various organisations in Singapore and India like Alchemy, QVT, Jefferies, ABN Amro and HSBC Securities. He Has a PhD in Economics from Tulane University, USA.