Why Dabur?

There are two main reasons:

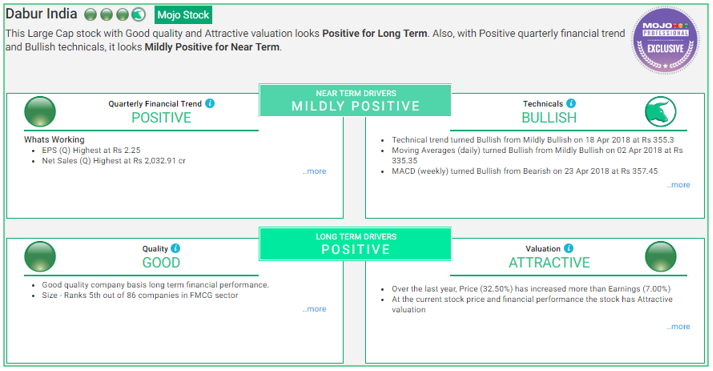

A) Based on our analysis, Dabur qualifies as a Mojo Stock.

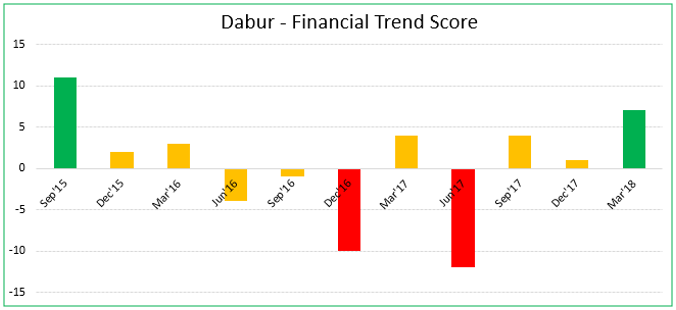

The Financial trend has recently turned around after a prolonged period where it was not positive.

B) In this current market (read more about that here) stocks which have high quality and whose downside is relatively protected will help protect one’s portfolio. FMCG stocks like Dabur generally fall in this category.

The 5 key Findings

In this piece, I have taken the Q4 FY18 Conference Call transcript posted on the Dabur website. I am looking for clues to figure out if the positive Financial Trend will continue for Dabur. Based on what the management of Dabur India, including CEO Mr Sunil Duggal, had to say in the Conference Call here are the findings.

1) The March quarter Improvement in Financial Trend is due to improvement in its Market share

Here is what the company says for the March quarter:

“Consolidated revenue from operations grew at 11.1%. Domestic FMCG business had like-to-like growth of 10%, driven by strong volume growth of 7.7%. Consolidated profit after tax reported growth of 18.9% for the quarter with operating margins increasing by 140 basis points on a comparable basis.”

Sunil Duggal, CEO, said that despite a subdued growth in the overall market, Dabur has grown because of gain in market-share.

“There have been very little tailwinds from the macros quite frankly as we speak. Category growths are still trending in the mid-single-digits at least for the large HPC categories, Oral, Skin, Hair Care, etc. There has been some uptick in March, but the fourth quarter has been fairly subdued, 5% – 6% volume growth. So obviously our volume growth which are trending at around 7% – 8% in these categories have come on the back of market share gains.”

Thus, “the last three quarters’ performance, especially this quarter and the last has been on the back of our own initiatives rather than on any support from the macros.”

2) Dabur benefits from Rural theme

The company in many places have talked about how they benefit from the rural economy.

The following statement is the crux:

“we see the urban growth has been around 8%, rural at around 13%, blended 10%. So rural continues to drive growth”

3) Dabur also benefits from the GST implementation

The company has very clearly said that while they have seen disruption due to GST implementation, but they gain a lot as things stabilize. Consider the following statements.

“I think GST net-net has been a big positive for us. There was a disruption that happened but it does lower our input cost, we get input credit benefits, especially in services area, our net worth improves, the unorganized competition reduces, all these are big positives.”

“After the GST implementation, the trade channels had seen some disruptions which seems to be stabilizing. We have seen good offtakes in the rural channels, Cash ‘n’ Carry, and organized retail. The year threw-up multiple challenges both in domestic and overseas which have been managed well and the year ended on a positive note.”

4) Dabur has pricing power

The company has enough pricing power to combat increase in raw material prices.

“Price increase will definitely happen, now it could be 2%, it could be 5%, I do not know. But that depends on how much inflation. But when I mention pricing power, so that means we have adequate amount of pricing headroom to deal with inflationary forces.”

5) It now expects the market to grow and that will be a tailwind

Consider the following statements which gives us clues on how they may do in the future:

“we do expect the category growth should trend up. While this may not be a certainty but there are indicators, especially in the form of monsoon which early trends indicates a normal monsoon, also a stimulus which we think will happen closer to elections. These should provide some momentum in terms of category growth.”

“We are pitching (the volume growth) internally at around 10%. Now like I said we do have a visibility of around 8% to 10% in the first half. The visibility in the second half is quite frankly not there, but in case category growths trend up to the high single-digits or thereabout, then I think we can do a low double-digit growth in the second-half, so the aggregate growth comes to 10%. That is what the internal thinking is and that may or may not happen, depends upon how well the disposable income in rural household trends up”

What gives comfort for long term is the following statement:

“Going forward, we will continue to invest strongly in our brand, distribution and infrastructure to continue to grow ahead of the market and enhance shareholder value.”

What does all this mean?

The findings help make the jigsaw a bit more complete. Dabur is already a Mojo stock and the management commentary is also fairly positive. Overall, this augurs well for the company.

Please Note:

There is lot more details in the conference call which dissects individual categories and the risks, I would urge you to read in full.

To help you in your own research and in our endeavour to make it information available to you on your fingertips, we have now bolstered our company section. For the companies that hold conference calls or post presentations, you can now access them on our site at the Company CV section. These include past calls and presentations as well.

Please also note that the above analysis on Dabur is just an illustration on how one can do more analysis using public information. This should not be taken as a recommendation.

Also Read:

Is ICICI the RCB of Private Banks?

Hero MotoCorp: The best Two-Wheeler Stock?

HDFC Bank: 5 Reasons the stock fits any portfolio

Happy Investing!

Sanjeev Mohta

Market Expert

Sanjeev Mohta is the Market Expert at Marketsmojo. He has over 27 years’ experience in Investment Research and Fund management across Asian Markets and Asset classes. He has worked in various organisations in Singapore and India like Alchemy, QVT, Jefferies, ABN Amro and HSBC Securities. He Has a PhD in Economics from Tulane University, USA.