“The explanation requiring the fewest assumptions is most likely to be correct.” William of Ockham

The Market Report Card

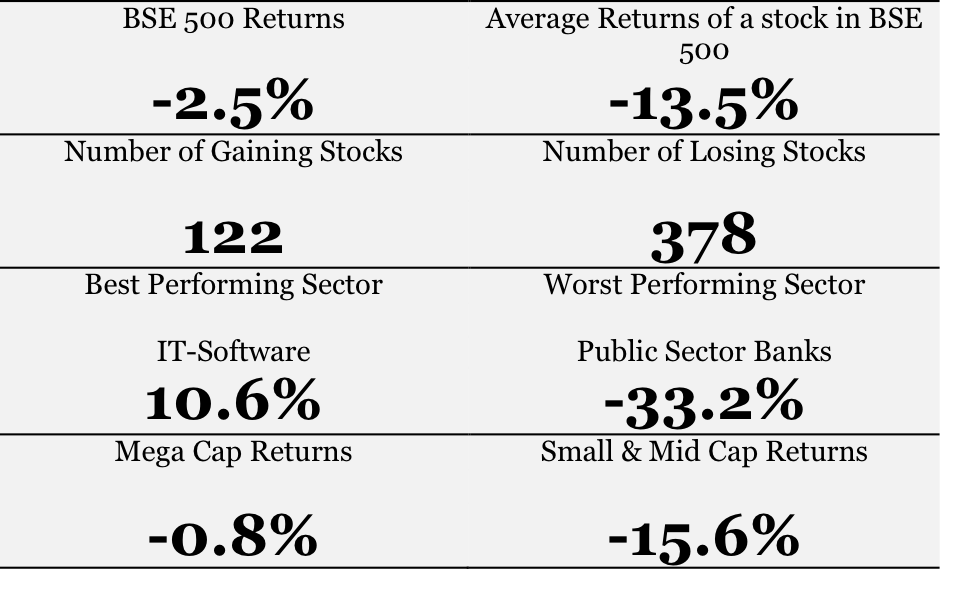

BSE 500 is a good Index as it includes 500 stocks across market cap and sector categories. For the period Jan-June 2018, the BSE 500 Report Card is not pretty.

The overall BSE 500 index as usual hides much more than it reveals. Behind the 2.5% fall there is completely different story.

- More than 75% stocks are down.

- if one looks at Small & Mid Cap stocks 80% are down.

- 85 stocks have lost at least a third of their Value.

So, Where is the market heading over the next six months?

Around Six weeks ago, I had written “How to Play these Tough Market Conditions” where I had pointed some of the factors which are impacting the market. The BSE Sensex has been pretty flat since then, although the smaller cap indices are down around 8%. Many of those factors remain.

As an update I present 6 factors, 2 Positive and 4 Negative, that are important to consider when trying to find an answer as to where the market is heading.

1) India’s Growth has normalised

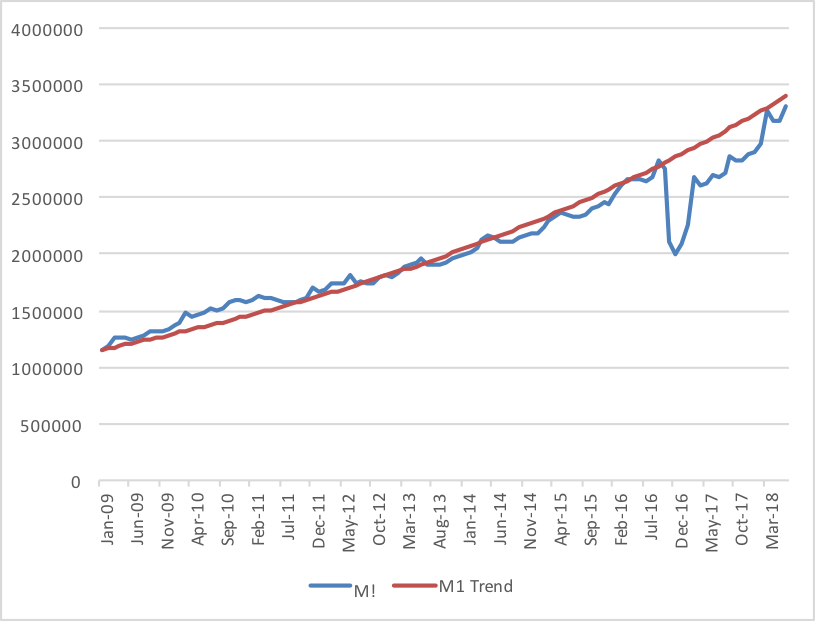

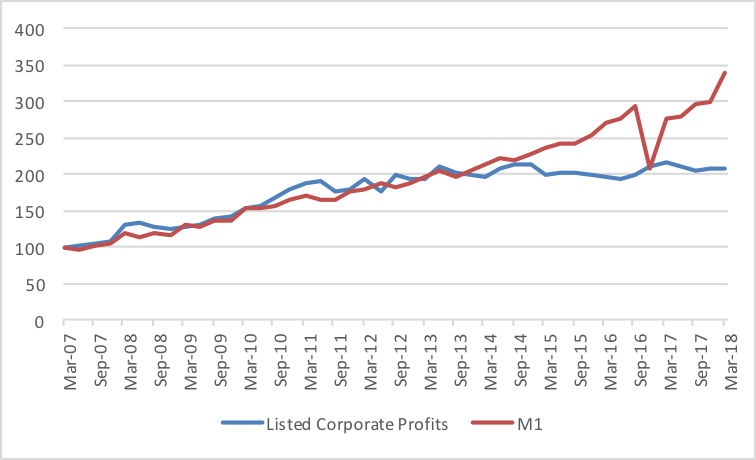

- M1 has caught up with its long-term trend.

M1, a narrow measure of Money Supply which takes into account Currency in Circulation and the Demand deposits with the bank, has been a good indicator of growth, not just for the economy but also for corporate India.

Over the last 10 years, M1 has grown by an average 12%. There was a dip in M1 due to Demonetisation but over the last few months M1 has caught up with the long-term trend growth.

- The one-off disruption from GST seems to have also reduced.

For example, Asian Paints in its latest Annual report said “In Q1 FY 2017-18, the paint industry experienced de-stocking following the GST rollout. In the succeeding three quarters, the industry gradually returned to normalcy.”

- The latest PMI data is also indicating improving growth.

According to a news report in Livemeint “India’s manufacturing sector activity in June grew at the strongest pace this year, supported by rise in domestic and export orders, according to a monthly survey. The Nikkei India Manufacturing Purchasing Managers Index (PMI) rose to 53.1 in June from 51.2 in May, registering the fastest improvement since December 2017. This is the 11th consecutive month that the manufacturing PMI remained above the 50-point mark—a score above 50 means expansion, while below that denotes contraction.”

2) The growth outlook is also getting better

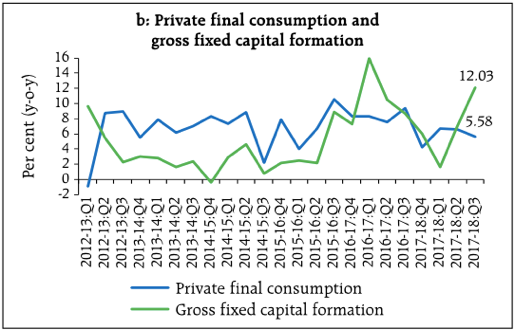

- The Gross Fixed Capital Formation has picked up. This is mainly due to government capex and this should help future growth.

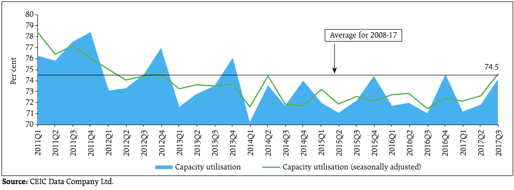

- The Capacity Utilisation has also normalised and over a period of time could lead to Corporations starting to invest in new capacities

- Good Monsoon means good rural growth

According to an article in Livemint, after remaining weak for more than 10 days, the south-west monsoon has quickly gained momentum to cover the entire country 17 days in advance. “Normally, the monsoon covers most parts of the country by 1 July, except extreme west Rajasthan, where there is high-variability and monsoon takes around 10-15 days to cover it. But this season it has advanced fast and covered even west Rajasthan by 29 June,” said M. Mohapatra, head (services) at India Meteorological Department (IMD).

3) Public Sector Banks woes set to continue

The stress in the banking sector continues as gross non-performing advances (GNPA) ratio rises further. According to RBI’s Financial Stability Report, GNPA ratio of all Banks put together may rise from 11.6 per cent in March 2018 to 12.2 per cent by March 2019. In fact for Public Sector Banks this ratio may increase from 15.6 per cent in March 2018 to 17.3 per cent by March 2019

Further for the 11 PSBs that are under the RBI’s PCA framework GNPA ratio could rise from 21.0 per cent in March 2018 to 22.3 per cent by March 2019, with 6 PCA PSBs likely experiencing capital shortfall.

Banking problems may limit financing needed for growth.

4) The External Factors are not favourable

- Higher current account deficit due to Higher Oil price and rising US interest rates could continue to cause problems for the Exchange Rate

Global Uncertainty and Fear of Trade wars will impact those currencies with higher current account deficit. The impact has already been seen on the Rupee to some extent.

- Emerging Markets are seeing Large Outflow

According to a report in MarketWatch “Investors, who flocked into emerging market equities and bonds at the beginning of the year, appeared to have given up on them since May. Redemptions from emerging market assets were $8 billion in May and $18 billion in June”

Given that Emerging markets are facing a huge outflow, India, one of the larger Emerging Market will not be insulated if this continues.Especially since India has a large FII participation.

5) Political Uncertainty remains

With Karnataka elections, which resulted in a hung assembly and a formation of a coalition government, Market has been a bit worried. To add to the uncertainty, there are more elections at the end of the year with states like MP, Rajasthan, Chattisgarh and Mizoram going for Elections. Also the General Elections will be held within the next one year. Political Uncertainty is set to continue as news flow regarding alliances etc making headlines.

While in the long term, I believe elections are less important, they will definitely play a role in the short-term market sentiment.

6) Valuations are not cheap

- Earnings growth has not kept up with Macro

Earnings which used to move with M1 (an indicator which I talked about above) have not kept pace with M1 for three years now as seen in the chart below.

- But the market went up, which made valuation expensive

In my piece, 4 Implications of the Current Market Valuations, I had highlighted the high valuations in the overall market.

The valuations are suggesting that the market believes earnings will catch up with macro soon. In a way, it is hoping that the one-off factors which have impacted earnings like Demonetisation, GST and Bank write offs are the main reason for the earnings to lag the macro factors and that they will fade and the earnings will catch up with macro.

This could happen. However, as long as the valuations remain expensive, the long-term return potential of the market gets impacted. Also, the ability for the market to weather unfavourable factors reduces. Thus, high valuations imply that market is more susceptible to uncertainties.

In conclusion

It is important to note that the state of the economy or politics are very difficult to predict. The good news is that Economic growth is moving in the right direction. Unfortunately, the mix of uncertainty of global flows, impact of possible trade wars and local political uncertainty are factors that cannot be ignored given the high valuations. The overall markets could remain tough for the near term, making this a stock pickers market.

What should we be doing in these markets? I will cover that in my next piece.

Also Read:

How to Play these Tough Market Conditions

The Playing Field: The FII Factor

4 Implications of the Current Market Valuations

Political Uncertainty Ahead… But Does Politics Matter?

Sanjeev Mohta

Market Expert

Sanjeev Mohta is the Market Expert at Marketsmojo. He has over 27 years’ experience in Investment Research and Fund management across Asian Markets and Asset classes. He has worked in various organisations in Singapore and India like Alchemy, QVT, Jefferies, ABN Amro and HSBC Securities. He Has a PhD in Economics from Tulane University, USA.